Cannabis operators have been known to be incredibly creative in their quest to protect their cash and reduce their tax liability. From management company structures, packaging markup deals, and even multi-entity setups, we’ve seen it all. But, there are instances where setting up a multi-entity structure can alleviate some of the tax burden caused by the 280E regulation. And let’s be honest, you want to be able to take some money out of your company and not get hammered on taxes at a personal level too.

In this article, we’ll walk you through an example of how a cannabis cultivation company has their business set up under one entity and their premises is owned by a secondary entity, and illustrate why this type of arrangement can be beneficial and what you need to consider. Owning property as a cannabis operator

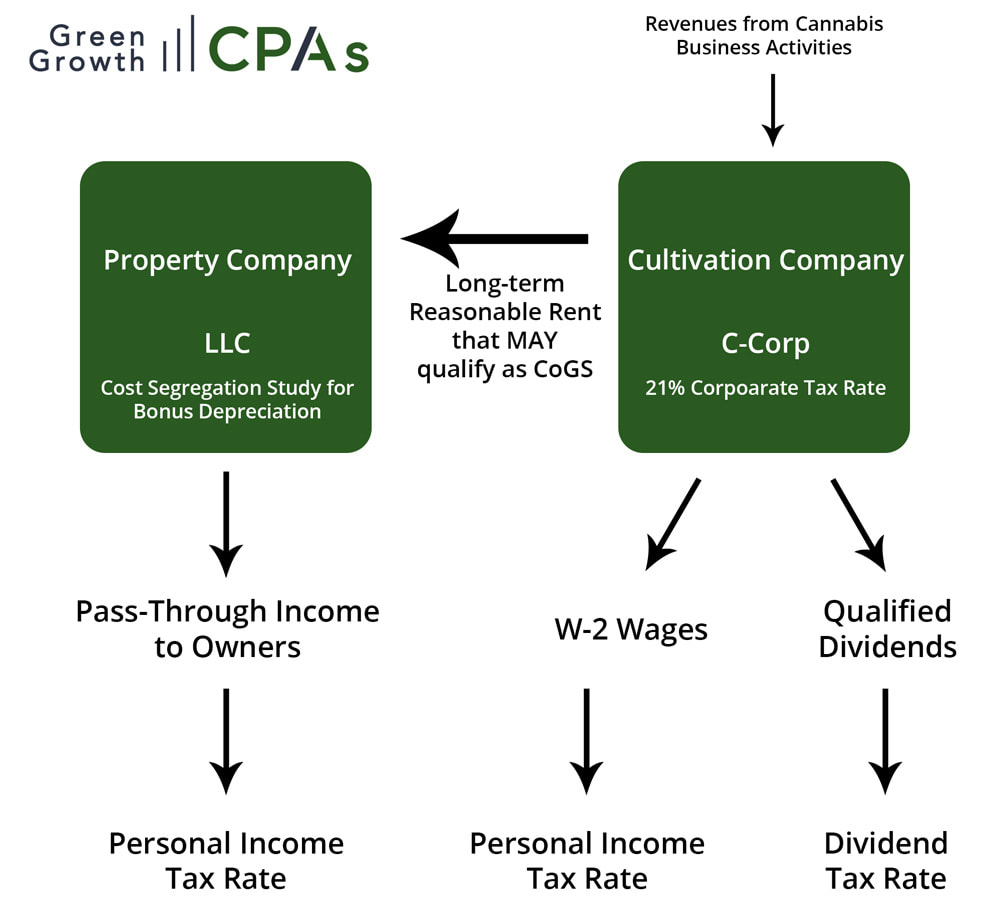

In this illustrative scenario, a cannabis cultivator leases the building in which their grow operation is based. The building is owned by a separate property business entity to protect the asset in case anything happens to or on the property.

So the first question we will answer is how do you set that building entity up, and who should own it? In most cases, you would establish an LLC as the property management company. An LLC is an appealing option because it creates a simple tax relationship: it is a pass-through entity with pass-through income. Compare this to an S-Corp election, which complicates things with respect to tax filings. Speak to a legal expert for your particular situation: there are some limitations to your liability as an LLC, and each operator has different needs. For this scenario, we’ll stick with an LLC structure for the property management company. The Property LLC offers a long-term lease to the cannabis cultivation business. Since it’s a rental property, and the income is considered passive, there will be no payroll tax on the property entity. Now, the more that you increase the rent, the more money you can take out of the cannabis cultivation operation to lessen your tax burden. Here’s how that works. Managing and moving cash between separate entities

For this set-up to work, there has to be “reasonable rent.” Reasonable rent is indicated by the market rate for a similar building and an arm’s length transaction. This essentially means that the property company and the cannabis cultivation business will act in their own self-interest to try to get the best deal they can and be reasonable at the same time. For instance, if the property charges $100/sq ft per month, that’s not considered “reasonable” – no cultivator would pay that rate.

Now here is a nuance that you need to consider. In the cannabis industry, due to green zoning regulations, there’s some wiggle room in what is considered “reasonable”; typically, cannabis businesses are forced to pay a markup due to high competition for relatively few compliantly zoned properties. That can equate to 1.5-3.5x normal market rents. The arrangement of one business paying the other is key for lowering your tax responsibility. Cash is taxed differently between the two businesses. LLCs are taxed differently than S-Corps or C-Corps, which is the typical entity structure chosen for cultivators. But, as a processing or cultivation business, you can take advantage of IRC 1-471. This regulation allows the cannabis business to write off that reasonable rent if it’s used for the production of the product. This rent cost goes right into your COGS. As a cultivator, this would likely be 90-95% of your rent that can be written off on your tax return. That rental income is then pass-through income to the property business ‘owners’ and tax is only paid on a personal level. Aside from only having to pay personal tax on the passive rental income, another tax strategy that the property business can take advantage of is bonus depreciation or a cost segregation study. A cost segregation study classifies certain leasehold improvements as equipment which allows you to use a shorter useful life to calculate depreciation. This means you can take bigger deductions faster as a property company. This can’t be done haphazardly; a cost segregation study must be conducted by a specialized team of engineers and CPAs. The result of this study helps limit the amount of tax that is assessed on the pass-through income. For example, if you have $500,000 in bonus depreciation for this year from the cost segregation study and $800,000 in rental income for this year, you will only be taxed on the $300,000 difference. Finally, as an added bonus for breaking costs into separate entities, M&A transactions become much easier. In the event that you wish to sell the building, you no longer have to worry about causing complications with your cannabis license. What entity should you choose as a cannabis cultivator?

A critical question to this whole arrangement is what type of business entity you should select for your cannabis cultivation business. There are a few different aspects you need to consider, including things like income levels, other streams of revenue, exit plans, risk tolerance, and more. We suggest that you speak to one of our CPAs for a complete analysis of your situation and the best way forward.

For illustrative purposes, let’s just talk about a few considerations you should keep in mind. First and foremost, remember that as a cannabis-touching company you are bound by the 280E tax code. This makes it difficult to create a good tax strategy and take money out of any cannabis business. S-Corps and C-Corps are two of the most common business entities so let’s look at considerations for each. In a C-Corps, you are taxed at a flat 21% thanks to the Tax Cuts and Jobs Act. Also, you can take money out of the business in two ways:

An S-Corp is a pass-through entity so there are no corporate taxes, but it does require a reasonable wage for each owner. If you choose to set up an S-Corps, then your goal is to keep this reasonable wage as low as possible to help mitigate self-employment tax on that wage at a personal level. Self-employment tax is a little over 15%; you could consider this as an additional tax.

Here is a quick example: imagine your $100 in reasonable wage is first taxed at self-employment rate which is 15.3%, and THEN the remaining money ($84.70) is then taxed at a federal income tax bracket level. The cannabis business could potentially write off some of this reasonable wage if it qualifies as COGS, but the self-employment tax could eat away at a personal level. The good news? The pass-through income of an S-Corp is not subject to self-employment tax. And lastly, you want to make sure that there is some clear delineation between the two or more entities. As we witnessed in the case of Alternative Health Care Advocates vs. the Commissioner of Internal Revenue, courts are not lenient in letting cannabis operators use “management companies” to mitigate their tax burden when they so closely intertwined with each other. Operators are trying to employ a multi-entity strategy to include certain business expenses on their tax return, and getting penalized for their efforts. Consider having different owners or managers for each business. What's the best multi-entity cannabis setup?

In short, there is no one-size-fits-all answer to creating a multi-entity tax structure. There are many considerations that you need to account for, and you should work with your CPA and a lawyer to figure out the best entity structure that will work for your business set up.

If you need help with this type of situation, we can run a financial model for you to help understand the implications of each strategy and choose the one that fits best for your situation. And, as circumstances change, your business may need to collaborate with us again to work out if any adjustments to the entity structure needs to be changed. Contact us today to get started.

|