2018 and the new tax code presents itself with a myriad of changes on both an individual and corporate level. One of the biggest changes, from a corporate level, was the elimination of the AMT (Alternative Minimum Tax). Today, we will talk about the definition of AMT, why it started and how it will impact the cannabis industry.

What is AMT? The corporate Alternative Minimum Tax (AMT) is a separate and distinct method of taxation that runs parallel to the “regular” corporate income tax. Prior to 2018, every corporation had to calculate its tax burden under both the regular corporate income tax and the AMT, paying the higher of the two. It’s important to note, today we will strictly be talking about AMT as it relates to corporations, not individuals (the AMT was not eliminated for individuals). The Alternative Minimum Tax began in 1969. The start of AMT can be traced to then Secretary of Treasury Joseph W. Barr. He testified before Congress that 155 individual taxpayers, with incomes exceeding $200,000, had paid no federal income tax in 1966. Adjusted for inflation, those numbers would translate to $1.5 million dollars today. The idea that the wealthiest citizens could pay zero income tax did not sit well with the government. Therefore, the AMT was created. This ensured that even those with higher incomes would pay a minimum amount of tax. Otherwise, through tax deductions and credits, citizens could essentially pay zero taxes. With so many deductions available, lawmakers wanted to ensure everyone paid at least some base minimum of tax regardless of how many tax breaks they could use to their advantage. Changes For 2018 Prior to the changes of 2018, the United States had one of the highest corporate tax rates in the world at 35%. The new 2018 regulations establish a flat 21% corporate rate for businesses and personal service corporations (PSCs). The corporate tax rate average for the developed world is 22%. Theoretically, the reduction of the corporate tax rate by 14% should create a nice boom for U.S. based companies, allowing them to keep their operations and profits here in the U.S. Prior to the changes for 2018, the corporate AMT tax rate was 20 percent. Additionally, C corporations with average gross receipts less than $7.5 million over the preceding three tax years were not subject to AMT. As of January 1, 2018 – the corporate AMT was completely eliminated. Individual AMT still applies, although a few things have changed. Please consult California Cannabis CPA if you’d like some guidance on individual AMT regulations. How Do These Changes Affect The Cannabis Industry? If your cannabis business is a corporation, you may benefit from the elimination of the AMT. If you are still researching how to set up your business, read our 10 steps to start a cannabis business. California Cannabis CPA is happy to walk you through the process. Theoretically, the removal of AMT should be a benefit. The AMT was a completely separate tax code that created a lot of additional record keeping. The elimination simplifies dozens of other tax code sections that were related to the corporate AMT. And unlike before, if your business made over a certain amount of money, you had to pay the higher of the two taxes. Not the case anymore. Second, functioning businesses are able to write off (or deduct) certain business expenses from their overall income. Normally, these include expenses such as operating costs, employee expenses and equipment. However, the cannabis business has certain limitations due to tax code 280E. On the federal level, cannabis is still considered a Schedule 1 drug. Therefore, licensed marijuana businesses have to file federal taxes under tax code 280E because of the Controlled Substances Act. The downside to filing under 280E is that licensed cannabis businesses pay more in federal taxes than other businesses do. 280E bans any tax deductions besides the cost of goods sold. If you try to deduct other expenses (similar to how other businesses operate) you will likely face an audit. However, there are situations where additional write-offs may be allowed. This is usually the case if your business participates in marijuana for medicinal purposes. 280E is a very complicated tax code, so we recommend consulting with California Cannabis CPA to ensure every detail is covered. In conclusion, it looks like the removal of the AMT will be beneficial, but cannabis companies will still run into challenges with the amount of expenses they are able to deduct. California Cannabis CPA is happy to speak with you to discuss your individual circumstance, ensuring you remain compliant with the new tax codes.  So, you want to start a business in California’s booming cannabis industry. Now seems like the perfect time to get in on the ground floor: the market estimates that cannabis will bring an additional $5 billion to California each year. It would be nice to get a slice of that pie, no?

Before you dive in, take some time to learn about the different ways to structure your business in a way that will give you the biggest slice of the pie -- not the leftover sliver that’s all crust (unless crust is your thing). The way you setup your company can mean the difference between growth and success and burning out after a year in business. Ask these five tax questions when setting out to structure your canna-business! 1. What kind of legal entity do you want to be? Historically, before California decided to have a fully regulated state system for medical marijuana, cannabis companies were set up as non-profits. Now, there are other options for structuring your business. Figuring out which model is right for you depends on many factors, including your role in the cannabis industry (i.e. grower, distributor, or partner); county and local regulations; and your projected growth. Here are some options available: Nonprofit (allowed pre-2018):

For profit (allowed in 2018):

2. What are your growth goals? Do you plan to have multiple locations and holdings? Depending on how your business operates, you can structure to account for different levels of liability. If you have multiple corporate entities, for example, you can limit your liability within each one. Then if one of your locations is sued or forced to shut down, your other locations can continue to operate independently. Conversely, managing multiple corporate entities can be a logistical nightmare -- especially if you intend to grow big or go home. It is much more efficient to run all your branches under one corporate entity if you’re smart about handling your risk. 3. What are your investors looking for? Investors will be interested in your company’s assets, inventory, cash receivables, and profit potential. They will want to see your business model in all its parts: trademarks, intellectual property, physical locations, and more. When you want to raise some serious capital -- going beyond your personal investment and a Kickstarter campaign -- the way you structure your company can impact an investor’s interest. For example, in a multi-entity structure with different locations and sub-companies, an investor can pick and choose which parts of your business they want to fund. Having a multi-entity structure can be very attractive if you’re shopping your canna-business around to people with low risk tolerance (and it widens your potential pool of funders). However, different ownership stakes can start to lead to conflicting interests for you as a manager. Having a seat at many tables with multiple influential voices can cause some real cross-company conflicts for you as a leader. 4. How should you structure compensation and benefits? Cannabis tax regulations have two special rules. First: cannabis companies can deduct the cost of goods sold on their tax return. Second: cannabis companies cannot deduct any sales and marketing expenses. Ouch. What this means is that many traditional expenses can’t be claimed as decreed by tax law section 280E. Know the ins and outs of payroll tax, executive compensation, and healthcare benefits you’ll be accountable for as a business owner in the California cannabis industry. The best way to do that is to consult with a tax professional in your community. 5. What do you need to do to be compliant? This is a big question -- and pretty broad at that. If you’ve made it this far, this step is the most crucial. Knowing what forms you need to fill out, what licenses you need, and how to best account for your expenses is what will make or break your business in the long run. California Cannabis CPA will be releasing more guides and checklists in the coming weeks to help you keep track of everything, but know that compliancy varies by district, county, and between the federal and state levels. If you’re going to have locations in different parts of California, do the research for each area you’re operating in. When in doubt -- pay your taxes!  Beginning January 1, 2018, the state of California’s marijuana tax laws will change for distributors, cultivators, manufacturers and retailers of marijuana and cannabis products. The information outlines the process for collecting, paying and filing taxes under the new laws: Step 1: Secure Permits and Licenses Step 2: Register with California Department of Tax and Fee Administration (CDTFA) Step 3: Collect and/or Pay Taxes Step 4: File Taxes Background: On November 8, 2016 voters in California approved Proposition 64 (Prop 64), the “Control, Regulate and Tax Adult Use of Marijuana Act”. This proposition was designed to reshape the use and taxation of marijuana in the state in a number of ways including designating specific agencies to regulate and licenses of the marijuana industry in California. Prop 64 also impacts the collection and payment of taxes for the following marijuana business groups defined below:

Step 1: Secure Permits and Licenses

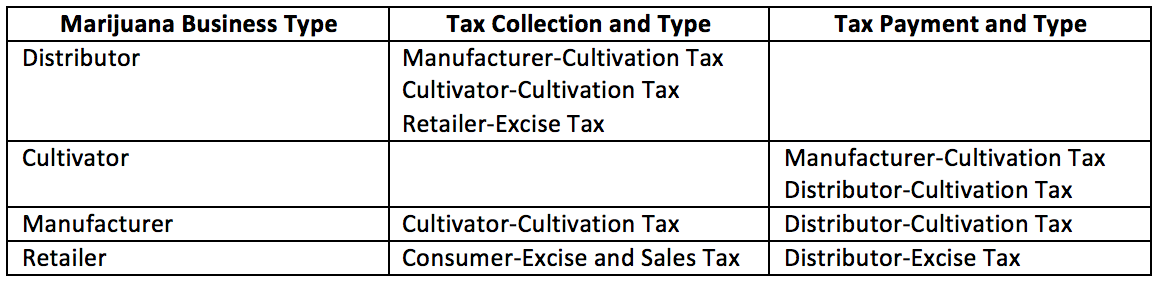

Under the new state law, marijuana businesses will be required to obtain licenses from the state agency listed above. The Bureau of Cannabis Control (BCC) is the agency developing regulations for medicinal marijuana use and those regulations should be available November 2017. Marijuana businesses are highly encouraged to apply for a temporary license from the BCC as soon as the regulations are available. The BCC will also issue temporary licenses which be effective January 1, 2018. In order to secure a temporary license through the BCC, a business must have authorization from a local government (city and/or county) to run a marijuana business in their local community. Temporary licenses will be good for 120 days from the date of issuance. This proposition imposes specific marijuana excise and cultivation taxes. Prop 64 was later amended by Senate Bill 94 (SB 94) which repealed the Medical Cannabis Regulation and Marijuana Safety Act (MCRSA) while defining the payment and collection of taxes. Below is the breakdown of tax collection and payment between distributors, cultivators, manufacturers and retailers:  Step 2: Register with California Department of Tax and Fee Administration (CDTFA): All marijuana distributors, cultivators, manufacturers and retailers are required to register with the CDTFA for seller’s and tax permits. Seller’s and tax permits are different and require that businesses apply for separate permits. Below is information that will be required for businesses to provide when registering with the CDTFA:

The NAICS number for most medicinal marijuana businesses is classified the same as pharmacies and drug stores therefore the code is 44610. Manufacturers may fall under a different NAICS code, depending on their business activities. The manufacturer section offers additional business code information on their NAICS classification. Distributor: Marijuana distributors must collect the following taxes: cultivation, excise and sales from the cultivators, manufacturers and retailers.

All business equipment and supplies (computers, signage, etc.) are generally subject to sales tax. Most retailers will collect the tax at the time of purchase. If the distributor is not taxed but the seller of the equipment, they should include the purchase on the “Purchases Subject to Use” tax on the “sales and use tax return”. Supplies like wrapping for marijuana and cannabis products (ex: bags) may fall under resale. The Tax and Fees section of the BOE offers additional information on use tax. Cultivator: The cultivator must pay the manufacturer and distributor a cultivation tax.

Please note that cultivation tax rate may change. Beginning January 1, 2020, the CDTFA will be required to annually adjust the cultivation tax rate based on inflation. The cannabis distributor, manufacturer and retailer must provide the cannabis cultivator with a “timely” and “valid” resale certificate. If a resale certificate is not provided a sales tax will be applied to the sale and the cannabis cultivator must report and pay tax to CDTFA. The California State Board of Equalization (BOE) offers additional information on sale for resale in Publication 103.

The following are examples of items considered cannabis cultivator farm equipment and machinery:

Cannabis cultivators who qualify for partial farm equipment exemptions may also qualify for partial exemption on solar power equipment. The state issued a special notice on solar power farm equipment offering additional details.

Manufacturer: The manufacturer must collect taxes from the cultivator and must pay the distributor a cultivation tax.

Please note that cultivation tax rate may change. Beginning January 1, 2020, the CDTFA will be required to annually adjust the cultivation tax rate based on inflation. Documentation like a receipt or invoice with the following information must be provided for these transactions. The information below should be included:

Retailer: The retailer charges and collects sales tax on “taxable retail sales” marijuana and cannabis products as well as other products. They are also required to collect cannabis excise tax from customers and pay this tax to the distributor. Sales:

Exemptions: Effective November 9, 2016 certain sales of medicinal marijuana are exempt from sales and use tax as defined by the Business and Professions code. Some items included are: medical cannabis, medicinal cannabis concentrate, edible medicinal cannabis products or topical cannabis. Customer must provide their MMI and ID at the time of purchase. Retailers must keep an electronic or paper record of the following information for exempt transactions:

Retailers should not collect sales tax on these purchases and should claim a deduction on sales and use tax return for exempt medicinal marijuana and cannabis products sales. Purchases: Purchases made on products that will be resold can be made without paying sales or use tax. Retailers must provide the seller a “valid” and “timely” resale certificate. Out-of-state vendors may not apply the California state tax. In this situation the cannabis retailer is responsible for reporting and paying the sales or use tax when they file their return with the CDTFA. Items for use in a retail business like signage, scales, and computers are subject to sales tax at the time of purchase. Packaging and other supplies may be purchased for resale without paying sales tax. Step 4: File Taxes: All marijuana business owners must register for a seller’s permit and file sales and use tax returns. Distributors of marijuana and cannabis products must register for a cannabis tax permit and file tax returns regularly.

As of November 9, 2016, certain retail transactions will be exempt from the sales and use tax. The BOE lists examples and the process for recording tax exempt transactions in a “Special Notice”.  Additional Information:

As a cannabis reseller or producer, you may have the option to deduct COGS for certain expenses related to the operation of your business. These deductions can offer some substantial tax savings for your business, as the deduction options for cannabis businesses are limited to COGS due to § 280E of the Internal Revenue Code (IRC).

When the IRS Office of Chief Counsel issued Chief Counsel Advice (CCA) 201504011 in 2015, this memo was designed to clarify the COGS deductions that are available to cannabis businesses. The IRS determined that the specific IRC sections that govern the items that can be included as COGS for cannabis businesses are §1.471-3(b), in the case of a cannabis reseller, and §1.471-3(c) and 1.471-11, in the case of a cannabis producer. While these regulations outline the general categories of deductions that are permitted for cannabis businesses, they do not detail what specific items cannabis businesses can deduct. To help you sort things out, here are some examples of the costs that you should include in your COGS basis for your canna-business so that you know exactly which items are deductible. COGS for Cannabis Resellers According to §1.471-3(b), the IRS has interpreted this section of the IRC to mean that cannabis businesses are permitted to deduct expenses related to inventory as COGS only. As result, cannabis resellers can claim deductions for: ●The invoice price for cannabis, less trade or other discounts ●Electric bills for designated inventory areas (electricity used in sales areas are not eligible to be deducted as COGS) ●Transportation (the cost of travel to purchase cannabis, transportation and shipping costs of the cannabis) Cannabis resellers are permitted to take these deductions only as long as these charges are strictly related to the acquisition of cannabis for resale and the storage and handling of inventory. The best way to ensure that the IRS will not challenge these deductions is by creating an inventory space that is closed off from the sales area of your cannabis business. COGS for Cannabis Producers For cannabis producers, §1.471-3(c) and § 1.471-11 of the IRC define how these businesses should treat cannabis production costs and define which expenses they are permitted to deduct as COGS. The IRC advises the use of the "full absorption" method of computing COGS which takes into account both direct and indirect production costs. Direct production costs are considered those costs which are necessary for the production of cannabis and the materials that are consumed as a part of the production process. Per the IRC, the direct production costs that cannabis producers can deduct are the costs of: ●Raw materials and supplies (seeds, soil, clones, fertilizer) ●Expenditures for direct labor (hiring workers to clean, trim, cure, package and inventory the cannabis and the associated wages, payroll taxes, and insurance) Examples of indirect production costs that can be deducted as COGS include: ●Repairs to production and storage facilities ●Maintenance costs for your production and storage facilities ●Utilities (water and electricity used to grow cannabis) ●Rent for your production facility ●Indirect materials and supplies (grow supplies and packaging) ●Indirect labor (supervisory wages) ●Costs of quality control and inspection These indirect production costs are only deductible if they can be related to the production of cannabis. In addition, if the cannabis production business prepares financial statements that are in accordance with GAAP, some additional expenses can be deducted, which are outlined here. Californians Helping to Alleviate Medical Problems (CHAMP) In a 2007 case, Caregiving Californians Helping to Alleviate Med. Problems, Inc. v. C.I.R., 128 T.C. 173, the Tax Court determined that CHAMP could take business deductions for the patient care portions of the non-profit’s medical marijuana dispensary operations. CHAMP was a caregiving program that was designed to provide members with medical cannabis in according with the laws of the state of California. The organization also provided one-on-one counseling, medical supplies, yoga instruction, healthy meals, and Internet access. As a not-for-profit entity per California law, the Tax Court agreed that CHAMP was actually two separate businesses. The ruling found that the CHAMP's primary business was actually caregiving services, which would permit the deduction of business expenses that were otherwise precluded by §280E. The CHAMP case made it possible for cannabis businesses to operate multiple businesses under one roof. As a result, it is a good idea to add additional services onto your cannabis business so that you can take advantage of as many of these COGS deductions as possible. Add patient services, such as counseling or advocacy, and make sure that all other businesses have real purposes and separate financial records to back up their operations. By expanding your business to include non-cannabis related services, you can improve your profits and increase the number of COGS deductions that your business can claim. Many cannabis-related businesses would like to take deductions for the costs related to their business activities. However, the tax code, Internal Revenue Code (“IRC”), has some very specific provisions regarding the businesses that are permitted to take cost of goods sold (COGS) deductions and which expenses may be included. COGS is at the core of all marijuana related businesses as its one of the key factors to reducing your taxable income.

Although figuring out which deductions are permitted can be tricky, it's in your best interest to claim all of the deductions that your business is allowed. COGS is a important deductions that marijuana-related businesses are allowed and can have a considerable effect on the effective tax rate for your business. Consider the following examples: Example 1. For a business with gross receipts totaling $776,772, a business with a high COGS could deduct $435,829, leaving a gross income of $340,953. Thanks to these allowed deductions, this business paid taxes on $340,953 instead of on $776,772. As a result, the business’s effective tax rate was 44% of its final earnings. Example 2. For a business with gross receipts totaling $776,772 and a low COGS with only $50,000 in COGS deductions, the gross income of the business was $726,772. Therefore, this business would pay taxes on $726,772. For this business, the effective tax rate was 94% of its final earnings. Simply taking COGS deductions rendered a 50% difference in the effective tax rate of each of these two businesses! As a result, claiming deductions for COGS could mean substantial tax savings for your business. Here is a quick guide to help you understand what COGS deductions are permitted for your cannabis-related business. Cannabis-related Businesses and Claiming COGS Although, cannabis-related businesses are currently illegal under federal law, every business in this industry is still obligated to pay federal income tax on its taxable income because IRC § 61(a) does not differentiate between income that has been earned from legal sources and income that has been earned from illegal sources. In 1982, Congress enacted § 280E, which prohibits deductions and credits for businesses trafficking in controlled substances. However, in a later case, Californians Helping to Alleviate Medical Problems, Inc., v. Commissioner, 128 T.C. 173 (2007) (“CHAMP”), the government acknowledged that § 280E does not prohibit a taxpayer from claiming COGS. In other cases involving non-medical marijuana or other Schedule I controlled substances, the Tax Court recognized that § 280E does not disallow adjustments to gross receipts for COGS. Chief Counsel Advice (CCA) 201504011 As a result of these rulings, the IRS determined that marijuana-related businesses could claim certain COGS deductions. On Jan. 23, 2015, the IRS Office of Chief Counsel issued Chief Counsel Advice (CCA) 201504011 to clarify that although deductions may not be claimed for trafficking marijuana, the CCA allows a cost-of-sales deduction for indirect production-related business expenses. The memo concluded that although marijuana-related businesses are permitted to determine COGS, they must do so using the § 280E as it was enacted in 1982 and § 471, which makes the provision for the use of inventories to determine business income. When §280E was enacted in 1982, an ‘inventoriable cost’ referred to any costs that could be capitalized to inventories under §471. Capitalization simply means delaying the recognition of an expense by treating the item as a fixed asset rather than recognizing the cost in the period that it was incurred. Capitalization is generally only used by companies that operate on the accrual basis of accounting. In addition, the IRS concluded that these businesses are not permitted to calculate COGS using the more recent IRS regulations which can be found in § 263A, which permitted the inclusion of additional expenses, namely purchasing, handling and storage expenses, and service costs. In order to claim any of the permitted deductions, the items must be “ordinary and necessary” within the meaning of § 162. IRC § 162 is one of the most important sections in the tax code because it defines what a deduction is. The IRC requires six different elements to claim an item as a business expense in order to claim a deduction. These elements are that the cost is: 1. Ordinary and necessary; 2. In carrying on; 3. A trade or business activity; 4. That it is an expense; and 5. That it was paid or incurred during the taxable year for which the return will be filed. The IRS findings explain what a deduction is and which expenses could be considered as COGS. Finally, it should be noted that the IRS concluded that the IRS has broad authority to require the marijuana-related business to change its method of accounting and to challenge the deductions claimed. What Expenses Can Be Considered as COGS? The IRS has made specific provisions for marijuana resellers versus producers. For Resellers CCA 201504011 clarified that, for resellers, the costs that they incur that are otherwise nondeductible under § 280E may not be deducted as COGS. These costs that are non-deductible are those that are directly related to the trafficking of marijuana. For resellers, this means that only the invoice price of purchased cannabis, less any trade or other discounts, as well as, the transportation and other costs necessary to gain possession of the inventory can be considered as COGS. For Producers For cannabis-production businesses, there are significantly more opportunities to claim items as COGS. Production-related wages, rents, and repair can be considered as COGS upon the sale of the inventory for accrual-basis taxpayers and immediately for cash-basis taxpayers that are cannabis-production businesses. However, marketing and general business expenses remain nondeductible. Indirect production costs that may be considered as COGS include: ● Repair expenses, ● Maintenance, ● Utilities, ● Rent, ● Indirect labor and production supervisory wages, including basic compensation, overtime pay, vacation and holiday pay, sick leave pay (other than payments pursuant to a wage continuation plan under section 105(d)), shift differential, payroll taxes and contributions to a supplemental unemployment benefit plan, ● Indirect materials and supplies, ● Tools and equipment not capitalized, and ● Costs of quality control and inspection, only if these costs are incident to and necessary for the production of cannabis. If these expenses are not related to cannabis production then they are nondeductible. The IRS has also permitted producers to claim some additional COGS deductions, as long as the company makes sure to produce financial statements that are in accordance with Generally Accepted Accounting Principles (GAAP). These expenses include: ● Taxes deductible under § 164, other than state, local, and foreign income taxes; ● Depreciation and depletion; ● Deductible employee benefits, including pension and certain profit sharing contributions, workers' compensation expenses, stock bonus plans, premiums on life and health insurance, and miscellaneous employee benefits such as safety, medical treatment, cafeteria, recreational facilities, and membership dues; ● Costs pertaining to strikes, rework labor, scrap, and spoilage; ● Administrative expenses related to production; ● Officers' salaries related to production; and ● Insurance costs related to production. While the provisions of the tax code do give some cannabis-related businesses the opportunity for some tax breaks, the IRS does not allow such businesses to take the same deductions as businesses in other industries. However, the repeal of § 280E of the IRC could make the burden lesser for cannabis-related businesses who have reported tax liabilities of up to 70% of their income. In addition, these rules could change at any time. Until the law changes, it is important for all businesses in this industry to establish proper record keeping in order to meet IRS requirements. If you have any questions, please feel free to contact us. |