Beginning January 1, 2018, the state of California’s marijuana tax laws will change for distributors, cultivators, manufacturers and retailers of marijuana and cannabis products. The information outlines the process for collecting, paying and filing taxes under the new laws: Step 1: Secure Permits and Licenses Step 2: Register with California Department of Tax and Fee Administration (CDTFA) Step 3: Collect and/or Pay Taxes Step 4: File Taxes Background: On November 8, 2016 voters in California approved Proposition 64 (Prop 64), the “Control, Regulate and Tax Adult Use of Marijuana Act”. This proposition was designed to reshape the use and taxation of marijuana in the state in a number of ways including designating specific agencies to regulate and licenses of the marijuana industry in California. Prop 64 also impacts the collection and payment of taxes for the following marijuana business groups defined below:

Step 1: Secure Permits and Licenses

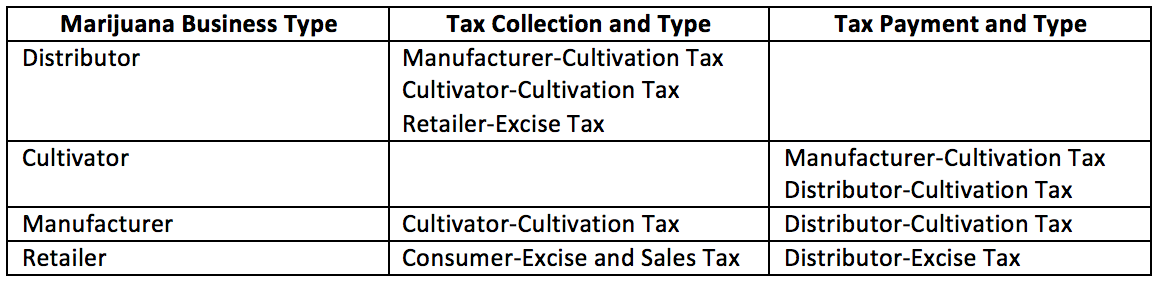

Under the new state law, marijuana businesses will be required to obtain licenses from the state agency listed above. The Bureau of Cannabis Control (BCC) is the agency developing regulations for medicinal marijuana use and those regulations should be available November 2017. Marijuana businesses are highly encouraged to apply for a temporary license from the BCC as soon as the regulations are available. The BCC will also issue temporary licenses which be effective January 1, 2018. In order to secure a temporary license through the BCC, a business must have authorization from a local government (city and/or county) to run a marijuana business in their local community. Temporary licenses will be good for 120 days from the date of issuance. This proposition imposes specific marijuana excise and cultivation taxes. Prop 64 was later amended by Senate Bill 94 (SB 94) which repealed the Medical Cannabis Regulation and Marijuana Safety Act (MCRSA) while defining the payment and collection of taxes. Below is the breakdown of tax collection and payment between distributors, cultivators, manufacturers and retailers:  Step 2: Register with California Department of Tax and Fee Administration (CDTFA): All marijuana distributors, cultivators, manufacturers and retailers are required to register with the CDTFA for seller’s and tax permits. Seller’s and tax permits are different and require that businesses apply for separate permits. Below is information that will be required for businesses to provide when registering with the CDTFA:

The NAICS number for most medicinal marijuana businesses is classified the same as pharmacies and drug stores therefore the code is 44610. Manufacturers may fall under a different NAICS code, depending on their business activities. The manufacturer section offers additional business code information on their NAICS classification. Distributor: Marijuana distributors must collect the following taxes: cultivation, excise and sales from the cultivators, manufacturers and retailers.

All business equipment and supplies (computers, signage, etc.) are generally subject to sales tax. Most retailers will collect the tax at the time of purchase. If the distributor is not taxed but the seller of the equipment, they should include the purchase on the “Purchases Subject to Use” tax on the “sales and use tax return”. Supplies like wrapping for marijuana and cannabis products (ex: bags) may fall under resale. The Tax and Fees section of the BOE offers additional information on use tax. Cultivator: The cultivator must pay the manufacturer and distributor a cultivation tax.

Please note that cultivation tax rate may change. Beginning January 1, 2020, the CDTFA will be required to annually adjust the cultivation tax rate based on inflation. The cannabis distributor, manufacturer and retailer must provide the cannabis cultivator with a “timely” and “valid” resale certificate. If a resale certificate is not provided a sales tax will be applied to the sale and the cannabis cultivator must report and pay tax to CDTFA. The California State Board of Equalization (BOE) offers additional information on sale for resale in Publication 103.

The following are examples of items considered cannabis cultivator farm equipment and machinery:

Cannabis cultivators who qualify for partial farm equipment exemptions may also qualify for partial exemption on solar power equipment. The state issued a special notice on solar power farm equipment offering additional details.

Manufacturer: The manufacturer must collect taxes from the cultivator and must pay the distributor a cultivation tax.

Please note that cultivation tax rate may change. Beginning January 1, 2020, the CDTFA will be required to annually adjust the cultivation tax rate based on inflation. Documentation like a receipt or invoice with the following information must be provided for these transactions. The information below should be included:

Retailer: The retailer charges and collects sales tax on “taxable retail sales” marijuana and cannabis products as well as other products. They are also required to collect cannabis excise tax from customers and pay this tax to the distributor. Sales:

Exemptions: Effective November 9, 2016 certain sales of medicinal marijuana are exempt from sales and use tax as defined by the Business and Professions code. Some items included are: medical cannabis, medicinal cannabis concentrate, edible medicinal cannabis products or topical cannabis. Customer must provide their MMI and ID at the time of purchase. Retailers must keep an electronic or paper record of the following information for exempt transactions:

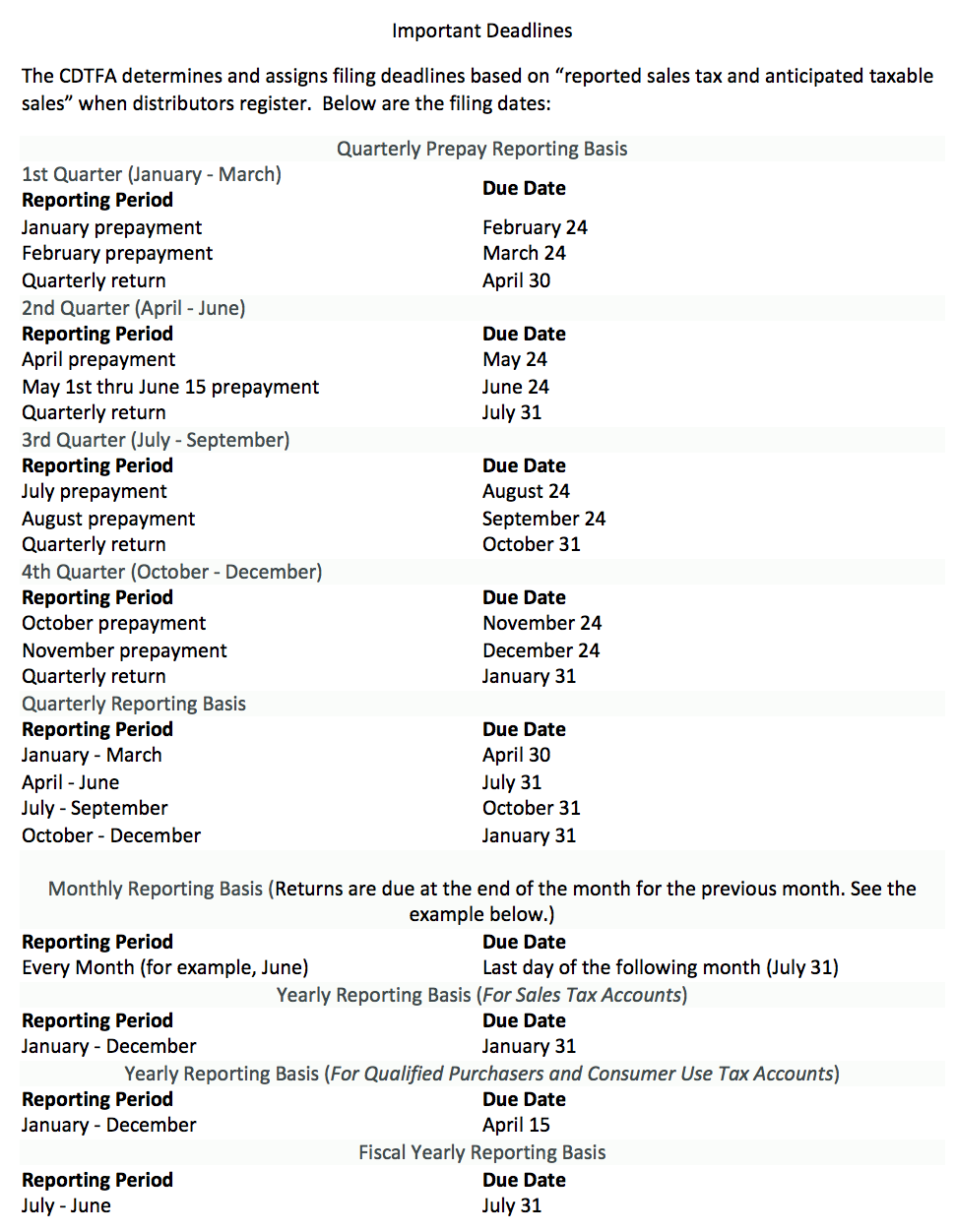

Retailers should not collect sales tax on these purchases and should claim a deduction on sales and use tax return for exempt medicinal marijuana and cannabis products sales. Purchases: Purchases made on products that will be resold can be made without paying sales or use tax. Retailers must provide the seller a “valid” and “timely” resale certificate. Out-of-state vendors may not apply the California state tax. In this situation the cannabis retailer is responsible for reporting and paying the sales or use tax when they file their return with the CDTFA. Items for use in a retail business like signage, scales, and computers are subject to sales tax at the time of purchase. Packaging and other supplies may be purchased for resale without paying sales tax. Step 4: File Taxes: All marijuana business owners must register for a seller’s permit and file sales and use tax returns. Distributors of marijuana and cannabis products must register for a cannabis tax permit and file tax returns regularly.

As of November 9, 2016, certain retail transactions will be exempt from the sales and use tax. The BOE lists examples and the process for recording tax exempt transactions in a “Special Notice”.  Additional Information:

|