An employee handbook, like any standard operating procedure (SOP), is useful for a variety of reasons. It can help you onboard new employees and train them on your company culture; it can create a common bond for cannabis dispensaries with multiple locations; and, worst-case scenario, it covers you in legal matters in the event you need to fire someone.

What few cannabis operators know is that there are actually some tax advantages to having a well-thought-out employee handbook. Here are some ways that having a great employee handbook at your cannabis business can save you money. Benefit 1: Reasonable methodology to claim employee hours for CoGS

The 280E tax code makes it impossible for cannabis operators to claim certain expenses other businesses would otherwise be able to deduct from their tax return.

Because cannabis remains a Schedule I classified substance, the only thing that cannabis operators are able to deduct from their taxes is CoGS – the cost of goods sold. CoGS refers to all costs involved in creating a product: for example, packaging, labeling, and raw materials. The IRS doesn’t define the way to allocate CoGS. As a result, cannabis operators must come up with their own system. Very sophisticated companies adopt technology and filing systems. They implement job codes for each task, tracked hours and even have a check-in and check out function for each room that employees are in. For a startup cannabis company, the employee handbook and job description serves as sufficient for developing a reasonable methodology for allocating employee time to CoGS. In the employee handbook or job description, list out all of the different expectations for each employee’s role. One of those requirements will delineate how an employee will be spending their time. For instance:

If you ever experience an audit, which is likely in cannabis, then you will have these documents, which we call audit additives. Triangulate your employee handbook with your CoGS allocations with respect to payroll expenses to justify your tax deductions. Benefit 2: Gross negligence protection

Cannabis businesses are cash-heavy. It’s imperative that you set and follow a large amount of SOPs around the movement of money and what you’re reporting to your accounting department and the government.

As we witnessed in the Alterman Case, a cannabis operator was given an accuracy-related penalty because they showed gross negligence in not keeping accurate records of cash movement within the company. In Alterman v. Commissioner, T.C. Memo 2018-83 a cannabis operator attempted to argue for a higher CoGS, but didn’t have a system in place to justify those claims. Instead, the court sided with the IRS’s narrow description of CoGS as “purchase costs plus production costs, and leaves out beginning inventory and ending inventory.” These same gross negligence problems can arise with investors: most operating agreements detail expectations on how accounting and reporting must happen within the company. Failing to follow the agreed-upon guidelines could end up with you being kicked out of a company. Do you want to really be kicked out for something that you can easily prevent? This is where your employee handbook plays a role. In the handbook, lay out the procedures that an employee will follow for various tasks that the IRS and investors will be looking at, including:

Of course, accidents happen, and something will come up because no organization is perfect. If you get audited, use the employee handbook and any relevant checks and balances you’ve installed. This shows that you have established policies and procedures and that employees knew what those policies and procedures were. This is the best you can do. In addition, make sure you’re conducting regular internal audits so these critical cash handling and accounting procedures are actually being followed. Benefit 3: Help with compliance and the employee/employer relationship

Hiring and firing employees are part of the job when you own a business. Having an employee handbook and job description can help make this part a bit more cut and dry. It sets a clear expectation and performance standard.

An employee handbook is more than just a reference manual for managers. “It explains expectations for everyone and mentions the consequences of violating these rules. By explaining workplace ethics and expected behavior with colleagues and the management, an employee handbook minimizes workplace disputes,” writes one HR expert. There are plenty of federal and state regulations around hiring and firing practices and avoiding discrimination. An employee handbook is a useful tool to consolidate those regulations in one place and lay them out in clear terms to protect your business. Have set guidelines for the steps to take if an employee is underperforming: are they placed on leave? Do they get a probationary period? Do they get put on a performance plan, and if so, what does that look like? Not only that, but it can save your HR team (if you have one) time from answering questions and onboarding new employees. Include information like:

Make sure your handbook is thorough and also easy to use. Once you have it in good shape, it can be used to guide your business for many years. If you need help with creating a cannabis business employee handbook, then please reach out to our team today!

We’ve offered guides for cannabis retailers and cannabis distributors, and here we cover tax responsibilities for cannabis cultivators and manufacturers. If you’ve been following our guides, many of these responsibilities will be familiar. Cannabis cultivators are anyone who grow, harvest, plant, dry, cure, grade, or trim the cannabis plant. If you are a nursery or cannabis plant processor, you are considered a cultivator. If you are someone who produces or prepares cannabis products, labels or re-labels cannabis containers, or who packages/repackages cannabis products, you are a manufacturer. Cultivators have to register for a seller’s permit with the CDTFA online at cdtfa.ca.gov. As a cultivator, when you make sales to other cannabis businesses, you will be required to get resale certificates, file sales and use tax returns, and report and pay use tax on taxable items purchased without tax and used by the cultivator. In addition, cannabis cultivators pay the cultivation tax to the distributor or manufacturer. In cases where unprocessed cannabis is first sold or transferred to a manufacturer, the manufacturer must collect the cultivation tax from the cultivator and pass it to the distributor for collection by the CDFTA. As a manufacturer, your responsibilities are similar to cultivators. You must also register for a seller’s permit, obtain resale certificates, file sales and use tax returns, and report and pay use tax on taxable items on taxable items purchased without tax and used by the manufacturer. Likewise, you are responsible for collecting cultivation tax from the cultivators and supplying a receipt if the unprocessed cannabis is transferred or sold to you first. Then, you will pay the cultivation tax to the distributor, who transfers the payment to the CDTFA. Be sure you keep proper records and have the right permits and licenses – in addition to a seller’s permit, both cultivators and manufacturers may need local or municipal-level licenses. We can help you sort out your licensing needs. Cultivation Tax This tax applies to all harvested cannabis that has entered the commercial market: that is, cannabis that has completed testing and complies with the quality assurance review as required by law. How much is cultivation tax? It depends on the type of cannabis products being sold.

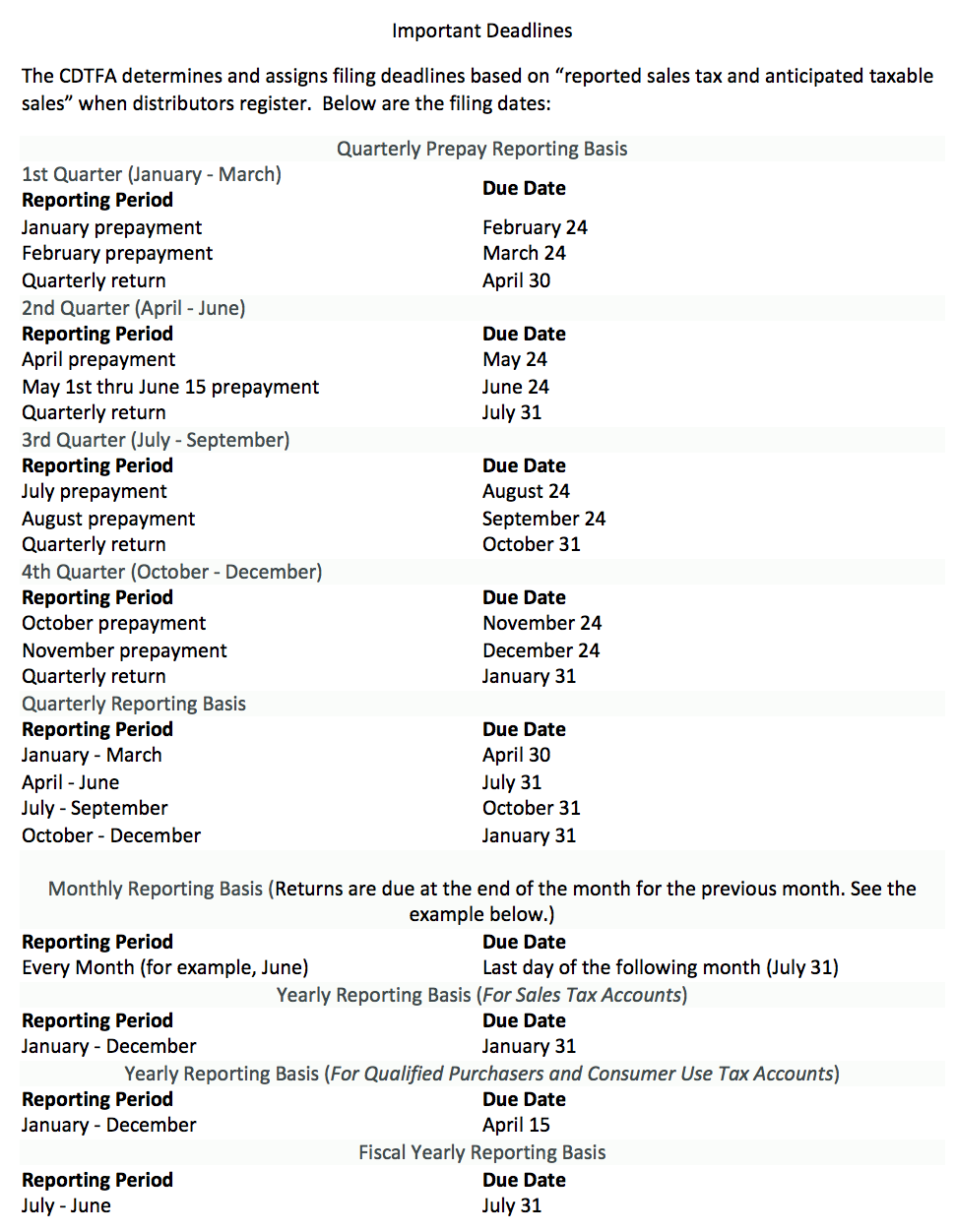

*Fresh cannabis plant fee only applies when the cannabis plant is weighed in an unprocessed state within 2 hours of harvesting. If you have immediate questions, please get in touch with our experts. Once again, distributors collect the cultivation tax from cultivators and manufacturers. Tax is due when the cannabis enters the commercial market. The distributor will provide an invoice or receipt when they collect the cultivation tax, and you should keep this for your records. Sales and Use Tax File your sales and use tax returns separate from your cannabis and income tax returns. Sales and use tax returns should be filed on the CDTFA website based on the due dates, which may vary. There are also some prepayments you will be asked to make which can be found on the same site. Keep copies of your returns in case there’s ever a question on your record-keeping. Sales tax applies to the retail sales of tangible personal property, including some labor or service costs if they are related to the sale of tangible property. Sales tax does not apply to valid sales for resale, though, so as a cultivator or manufacturer, virtually all your sales should be for resale (meaning your sales tax responsibilities are negligible). When you make a resale, use Form CDTFA-230 as your resale certificate. Don’t use a resale certificate for any personal property – you may be penalized! Use tax is a tax on all items that you use and consume and purchased without paying tax. In the real world, this might include getting a massage – it was a service you used that likely didn’t include tax when you originally paid the masseuse. Use tax is the same rate as sales tax and will generally apply to purchased from outside California that you didn’t pay state tax on at the time of purchase. These tax responsibilities can seem overwhelming, but that’s where our experts come in to help. If you have any questions pertaining to cultivation, sales, or use tax, please don’t hesitate to get in touch. We’re here to help you stay compliant!  Beginning January 1, 2018, the state of California’s marijuana tax laws will change for distributors, cultivators, manufacturers and retailers of marijuana and cannabis products. The information outlines the process for collecting, paying and filing taxes under the new laws: Step 1: Secure Permits and Licenses Step 2: Register with California Department of Tax and Fee Administration (CDTFA) Step 3: Collect and/or Pay Taxes Step 4: File Taxes Background: On November 8, 2016 voters in California approved Proposition 64 (Prop 64), the “Control, Regulate and Tax Adult Use of Marijuana Act”. This proposition was designed to reshape the use and taxation of marijuana in the state in a number of ways including designating specific agencies to regulate and licenses of the marijuana industry in California. Prop 64 also impacts the collection and payment of taxes for the following marijuana business groups defined below:

Step 1: Secure Permits and Licenses

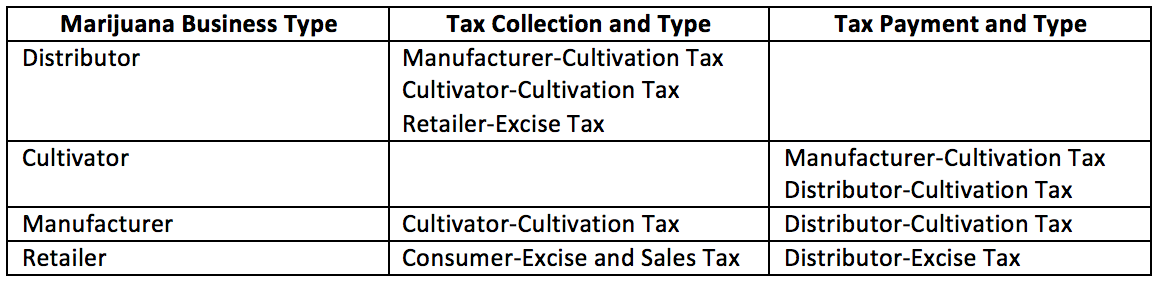

Under the new state law, marijuana businesses will be required to obtain licenses from the state agency listed above. The Bureau of Cannabis Control (BCC) is the agency developing regulations for medicinal marijuana use and those regulations should be available November 2017. Marijuana businesses are highly encouraged to apply for a temporary license from the BCC as soon as the regulations are available. The BCC will also issue temporary licenses which be effective January 1, 2018. In order to secure a temporary license through the BCC, a business must have authorization from a local government (city and/or county) to run a marijuana business in their local community. Temporary licenses will be good for 120 days from the date of issuance. This proposition imposes specific marijuana excise and cultivation taxes. Prop 64 was later amended by Senate Bill 94 (SB 94) which repealed the Medical Cannabis Regulation and Marijuana Safety Act (MCRSA) while defining the payment and collection of taxes. Below is the breakdown of tax collection and payment between distributors, cultivators, manufacturers and retailers:  Step 2: Register with California Department of Tax and Fee Administration (CDTFA): All marijuana distributors, cultivators, manufacturers and retailers are required to register with the CDTFA for seller’s and tax permits. Seller’s and tax permits are different and require that businesses apply for separate permits. Below is information that will be required for businesses to provide when registering with the CDTFA:

The NAICS number for most medicinal marijuana businesses is classified the same as pharmacies and drug stores therefore the code is 44610. Manufacturers may fall under a different NAICS code, depending on their business activities. The manufacturer section offers additional business code information on their NAICS classification. Distributor: Marijuana distributors must collect the following taxes: cultivation, excise and sales from the cultivators, manufacturers and retailers.

All business equipment and supplies (computers, signage, etc.) are generally subject to sales tax. Most retailers will collect the tax at the time of purchase. If the distributor is not taxed but the seller of the equipment, they should include the purchase on the “Purchases Subject to Use” tax on the “sales and use tax return”. Supplies like wrapping for marijuana and cannabis products (ex: bags) may fall under resale. The Tax and Fees section of the BOE offers additional information on use tax. Cultivator: The cultivator must pay the manufacturer and distributor a cultivation tax.

Please note that cultivation tax rate may change. Beginning January 1, 2020, the CDTFA will be required to annually adjust the cultivation tax rate based on inflation. The cannabis distributor, manufacturer and retailer must provide the cannabis cultivator with a “timely” and “valid” resale certificate. If a resale certificate is not provided a sales tax will be applied to the sale and the cannabis cultivator must report and pay tax to CDTFA. The California State Board of Equalization (BOE) offers additional information on sale for resale in Publication 103.

The following are examples of items considered cannabis cultivator farm equipment and machinery:

Cannabis cultivators who qualify for partial farm equipment exemptions may also qualify for partial exemption on solar power equipment. The state issued a special notice on solar power farm equipment offering additional details.

Manufacturer: The manufacturer must collect taxes from the cultivator and must pay the distributor a cultivation tax.

Please note that cultivation tax rate may change. Beginning January 1, 2020, the CDTFA will be required to annually adjust the cultivation tax rate based on inflation. Documentation like a receipt or invoice with the following information must be provided for these transactions. The information below should be included:

Retailer: The retailer charges and collects sales tax on “taxable retail sales” marijuana and cannabis products as well as other products. They are also required to collect cannabis excise tax from customers and pay this tax to the distributor. Sales:

Exemptions: Effective November 9, 2016 certain sales of medicinal marijuana are exempt from sales and use tax as defined by the Business and Professions code. Some items included are: medical cannabis, medicinal cannabis concentrate, edible medicinal cannabis products or topical cannabis. Customer must provide their MMI and ID at the time of purchase. Retailers must keep an electronic or paper record of the following information for exempt transactions:

Retailers should not collect sales tax on these purchases and should claim a deduction on sales and use tax return for exempt medicinal marijuana and cannabis products sales. Purchases: Purchases made on products that will be resold can be made without paying sales or use tax. Retailers must provide the seller a “valid” and “timely” resale certificate. Out-of-state vendors may not apply the California state tax. In this situation the cannabis retailer is responsible for reporting and paying the sales or use tax when they file their return with the CDTFA. Items for use in a retail business like signage, scales, and computers are subject to sales tax at the time of purchase. Packaging and other supplies may be purchased for resale without paying sales tax. Step 4: File Taxes: All marijuana business owners must register for a seller’s permit and file sales and use tax returns. Distributors of marijuana and cannabis products must register for a cannabis tax permit and file tax returns regularly.

As of November 9, 2016, certain retail transactions will be exempt from the sales and use tax. The BOE lists examples and the process for recording tax exempt transactions in a “Special Notice”.  Additional Information:

The IRS is getting tough on cannabis business in Colorado and is going after cannabis entrepreneurs who failed to fill out Form 8300. If you want to avoid being audited by the IRS, it is important for you to stay on top of these filings. Here is what Form 8300 is and why it is important.

What Is Form 8300? Form 8300, Report of Cash Payments Over $10,000 Received in a Trade or Business, is a form used by the federal government to keep track of cash payments of more than $10,000. These filings are designed to assist law enforcement in investigating and preventing money laundering, tax evasion, drug dealing, financing of terrorism activities, and other criminal acts. For purposes of Form 8300, cash doesn't only include U.S. dollar coins and bills and foreign currency notes; it may also include cashier's checks, bank drafts, traveler's checks, and money orders if the face value is $10,000 or less. These filings are designed to assist law enforcement in investigating and preventing money laundering, tax evasion, drug dealing, financing of terrorism activities, and other criminal acts. Who Must File Form 8300? Every person who engages in a trade or business and also receives more than $10,000 in cash in a single transaction or in two or more related transactions is required to file Form 8300. Transactions that are considered related transactions are those that are conducted between a payer (or its agent) in a 24-hour period. The transactions may also be considered related if the recipient of the payment knows that each transaction is a part of a series of transactions. The IRS has also issued IRS Form 8300 Reference Guide to help you determine which transactions qualify as reportable transactions. Cash doesn't only include U.S. dollar coins and bills and foreign currency notes. It may also include cashier's checks, bank drafts, traveler's checks, and money orders if the face value is $10,000 or less. Form 8300 Filing Examples Here are two examples to help you understand when you need to file Form 8300: Example 1. Jack asks an employee to purchase cannabis for his dispensary. The employee orders the product in two shipments and he pays with two cash payments, each for $6,000. The cannabis grow business who received more than $10,000 in the designated reporting transaction must file Form 8300. Example 2. A cannabis supply shop sells growing equipment for $9,000 in cash to Adam at 10 a.m. During the afternoon on the same day, Adam returns to buy more equipment and pays an additional $9,000 in cash. Since, both transactions occurred within a 24-hour period, they are related transactions and the grow equipment supplier must file Form 8300. When Do I File Form 8300? Each time you receive a payment that meets the criteria for filing Form 8300, you must file the form for the transaction within 15 days of receiving the payment. You can file online using the Bank Secrecy Act (BSA) Electronic Filing (E-Filing) System at the FinCEN website. What Are the Penalties for Failing to File Form 8300? If you simply fail to file Form 8300 on time, a penalty of $250 per occurrence will be assessed. This penalty is capped at $1,000,000 per year for businesses with gross receipts not exceeding $5 million. If you fix the error and make sure that the forms are filed within 30 days of the deadline, then this penalty limited is reduced to $175,000 per year for businesses with gross receipts not exceeding $5 million. However, if your business grosses more than $5 million, then the penalty cap increases to $3 million. However, if you intentionally fail to file Form 8300, the penalty increases to $25,000 of the total amount of the transaction, up to a maximum of $100,000 for each time that you failed to file. In addition, felony charges may be brought against you in more severe cases. Criminal penalties will be applied by default if you structure or appear to structure payments in order to avoid filing Form 8300 for the transactions. |