An employee handbook, like any standard operating procedure (SOP), is useful for a variety of reasons. It can help you onboard new employees and train them on your company culture; it can create a common bond for cannabis dispensaries with multiple locations; and, worst-case scenario, it covers you in legal matters in the event you need to fire someone.

What few cannabis operators know is that there are actually some tax advantages to having a well-thought-out employee handbook. Here are some ways that having a great employee handbook at your cannabis business can save you money. Benefit 1: Reasonable methodology to claim employee hours for CoGS

The 280E tax code makes it impossible for cannabis operators to claim certain expenses other businesses would otherwise be able to deduct from their tax return.

Because cannabis remains a Schedule I classified substance, the only thing that cannabis operators are able to deduct from their taxes is CoGS – the cost of goods sold. CoGS refers to all costs involved in creating a product: for example, packaging, labeling, and raw materials. The IRS doesn’t define the way to allocate CoGS. As a result, cannabis operators must come up with their own system. Very sophisticated companies adopt technology and filing systems. They implement job codes for each task, tracked hours and even have a check-in and check out function for each room that employees are in. For a startup cannabis company, the employee handbook and job description serves as sufficient for developing a reasonable methodology for allocating employee time to CoGS. In the employee handbook or job description, list out all of the different expectations for each employee’s role. One of those requirements will delineate how an employee will be spending their time. For instance:

If you ever experience an audit, which is likely in cannabis, then you will have these documents, which we call audit additives. Triangulate your employee handbook with your CoGS allocations with respect to payroll expenses to justify your tax deductions. Benefit 2: Gross negligence protection

Cannabis businesses are cash-heavy. It’s imperative that you set and follow a large amount of SOPs around the movement of money and what you’re reporting to your accounting department and the government.

As we witnessed in the Alterman Case, a cannabis operator was given an accuracy-related penalty because they showed gross negligence in not keeping accurate records of cash movement within the company. In Alterman v. Commissioner, T.C. Memo 2018-83 a cannabis operator attempted to argue for a higher CoGS, but didn’t have a system in place to justify those claims. Instead, the court sided with the IRS’s narrow description of CoGS as “purchase costs plus production costs, and leaves out beginning inventory and ending inventory.” These same gross negligence problems can arise with investors: most operating agreements detail expectations on how accounting and reporting must happen within the company. Failing to follow the agreed-upon guidelines could end up with you being kicked out of a company. Do you want to really be kicked out for something that you can easily prevent? This is where your employee handbook plays a role. In the handbook, lay out the procedures that an employee will follow for various tasks that the IRS and investors will be looking at, including:

Of course, accidents happen, and something will come up because no organization is perfect. If you get audited, use the employee handbook and any relevant checks and balances you’ve installed. This shows that you have established policies and procedures and that employees knew what those policies and procedures were. This is the best you can do. In addition, make sure you’re conducting regular internal audits so these critical cash handling and accounting procedures are actually being followed. Benefit 3: Help with compliance and the employee/employer relationship

Hiring and firing employees are part of the job when you own a business. Having an employee handbook and job description can help make this part a bit more cut and dry. It sets a clear expectation and performance standard.

An employee handbook is more than just a reference manual for managers. “It explains expectations for everyone and mentions the consequences of violating these rules. By explaining workplace ethics and expected behavior with colleagues and the management, an employee handbook minimizes workplace disputes,” writes one HR expert. There are plenty of federal and state regulations around hiring and firing practices and avoiding discrimination. An employee handbook is a useful tool to consolidate those regulations in one place and lay them out in clear terms to protect your business. Have set guidelines for the steps to take if an employee is underperforming: are they placed on leave? Do they get a probationary period? Do they get put on a performance plan, and if so, what does that look like? Not only that, but it can save your HR team (if you have one) time from answering questions and onboarding new employees. Include information like:

Make sure your handbook is thorough and also easy to use. Once you have it in good shape, it can be used to guide your business for many years. If you need help with creating a cannabis business employee handbook, then please reach out to our team today!

As you know, cannabis operators have to pay many different taxes.

From sales tax to excise tax, the system is quite complex; and once your cannabis company starts to thrive, the tax system becomes even more complicated. California’s sales tax is a great example of where successful cannabis entrepreneurs get tripped up with being compliant while maximizing their profit. California’s state sales tax for cannabis operators is 7.25% – 6% state tax, plus a 1.25% mandatory local tax. Depending on where your business is located, the local tax may be an additional 3% to well over 10%. For cannabis operators who are achieving a certain amount of sales each month, you will be required to pay the sales tax monthly, rather than quarterly. Here’s how the process works, and how our experts can help you manage your tax burden more effectively. Why is proper tax reporting important?

As the saying goes, there are two things certain in life: death and taxes.

Taxes are the number one reason why most cannabis companies fail; the IRS is not shy about auditing cannabis operators, and the 280E is one of the primary tools the government uses to penalize cannabis ventures. This burdensome 280E regulation makes a lot of money for the IRS in the form of fees and fines; so much so that Colorado is able to fix roads that aren’t even broken because they have so much tax revenue. It’s important to protect you business as much as possible from the tax authorities; and the first step is to understanding cannabis sales tax and commit to paying your taxes monthly. As a side note: having a CPA prepare your taxes is best because they will use an accepted methodology for their calculations that can then be used as exhibits during a potential audit. What is cannabis sales tax?

As previously mentioned, the state sales tax rate varies slightly depending on where you are. Most cannabis organizations can expect to pay 8% - 10% of sales. Sales tax is charged at the cannabis dispensary on top of the sales price and the cannabis business tax. Here is a breakdown of cannabis tax calculations for California.

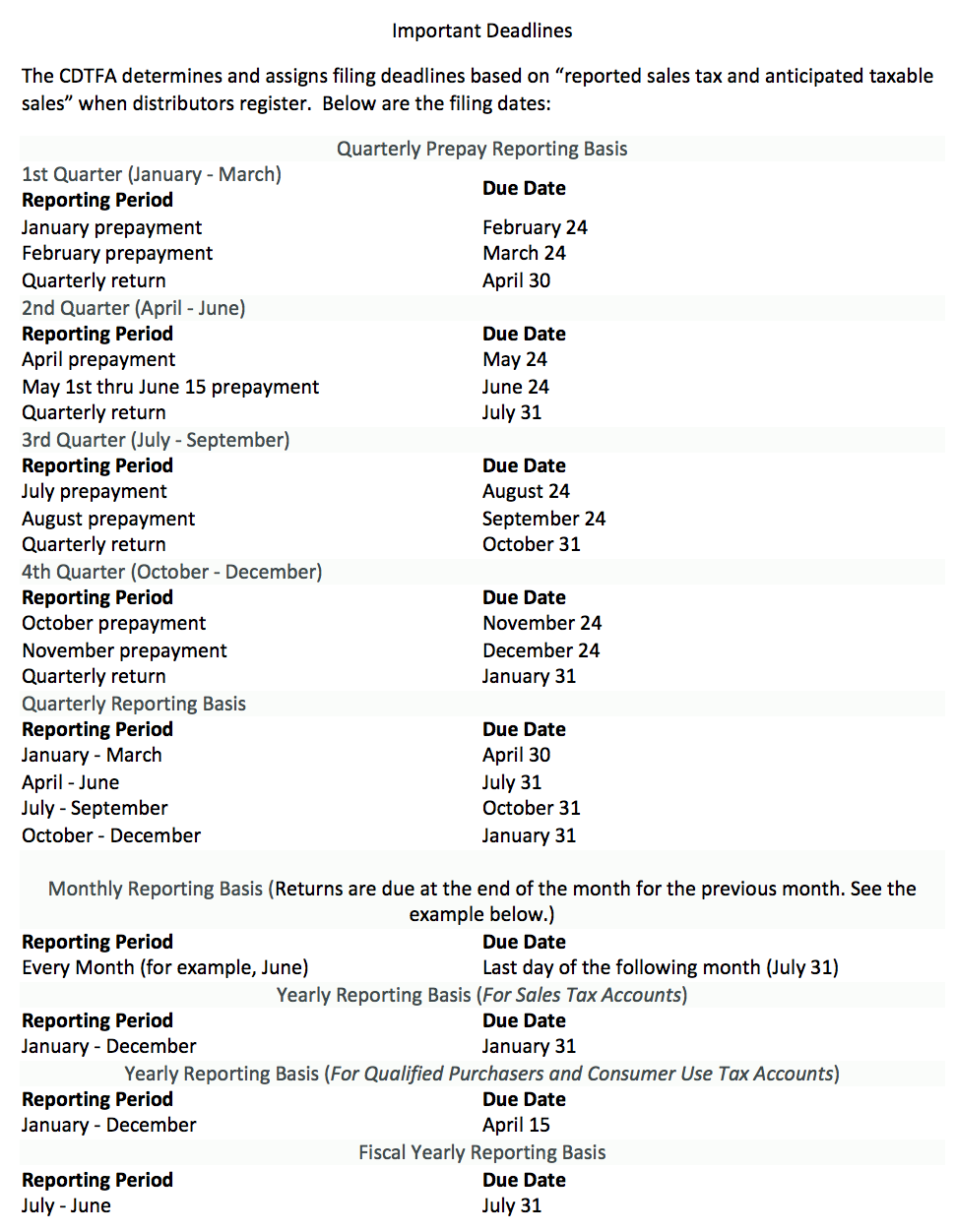

Cannabis sales tax in California is paid to the CDTFA. When you apply for a sales tax permit, the Administration will ask you a series of questions to see what your payment schedule should be. Typically, most companies pay their taxes quarterly – meaning that taxes are due April 30, July 31, October 31, and January 31 for the periods Q1, Q2, Q3, and Q4 (respectively). If you have low sales volume (meaning less than $5,000 in sales), the CDTFA may put you on an annual payment schedule. For successful, high sales organizations, it’s likely that you will be asked to pay sales tax monthly to the city and state. Here’s what that process looks like and why it’s best to have an experienced CPA calculate your payments for you. How to calculate sales tax for the state

In our experience, some clients are asked to pre-pay sales tax every single month because they have such high cannabis sales. How does this work?

In this instance, the cannabis operator must pay estimated payments for month one and month two of the quarter. Then, when the quarterly return is filed, the CPA firm squares up discrepancies from the first two months of the quarter into the third month’s payment. How do we estimate your month one and two sales? The GreenGrowth CPAs usually look at your POS software on the 20th day of the month to see your current run rate, and in addition compare that rate to the past year for the month we are evaluating. From there, we create an estimate of the monthly of ABC$$ to the CDTFA, thereby covering your state taxes. The CDTFA will now let you know that you are subject to pre-payments or any changes to the frequency of your payments. If you don’t make payments on time, then penalties and interest will be assessed. Note that these penalties are compounding – so if you are faced with a fine, pay it right away. How to calculate sales tax for your local jurisdiction

In addition to paying your state sales tax, cannabis operators must also pay city sales tax. This rate and due date varies depending on your location.

For example, if you are based in the city of Vallejo, you are required to file a monthly return based on gross receipts, rather than sales. These are due by the 20th or 25th of the following month. Get in touch with our experts or the local tax authority to make sure you know the deadline and cannabis sales tax rate you are responsible for. There’s a lot of confusion and grey area when preparing for your tax payments to the city – mostly because cannabis is an all-cash industry, and most cities aren’t equipped to process monthly payments of cash. Most cities have self-reporting taxes with no audits required (yet). It’s likely, however, that California cities are missing out on major tax revenue, and as a result will insist on proper reporting and auditing in the future. It’s best to be rigorous about your tax payments to make sure there are no issues down the road. How can you make sure you’re paying the right amount? Make sure you’re instituting great cash-handling practices and create strong SOPs. Despite having little to no access to a bank account, manage your cash responsibly to make sure everything balances correctly. Plan ahead: if you're looking at your cash or bank account, start setting up an account or repository for taxes. Put money aside each week so that you’re not forced to come up with a large sum of cash all at once. To give yourself total peace of mind, engage an accountant with specific cannabis-industry experience who can give you monthly guidance and be by your side in the event that you get audited by the city, state or federal government. Click the button below to get started with one of our experts.

The recreational cannabis industry is considered a high-growth market, with the potential to grow to $66.3 billion by 2025.

However, despite the massive amount of cash pouring into the industry, operators are limited by the Cole Memorandum and federal regulations prohibiting banks from working with cannabis companies. Lack of access to the banking system causes many problems for legal cannabis businesses – especially when it comes to paying taxes. Federal regulations force cannabis operators to pay their taxes in cash (in most cases). There are a lot of cannabis taxes to be accounted for; the US government is estimated to have collected $4.7 billion in taxes from cannabis companies in 2017. That’s not to mention the state and local taxes cannabis operators are subject to – which can be at rates as high as 15% in some areas. Cannabis operators want to pay their taxes, but the rules regarding how to submit payment make it a headache. The transfer of cash is not only frustrating and difficult, but often risky. Handling that much cash presents a big personal safety risk for cannabis business owners and the agencies collecting the cash. So the question remains, how can cannabis operators better navigate the tax return process given federal banking restrictions? Let's explore the process... EFTPS and Federal Taxes

Generally speaking, ordinary corporations and C-Corps pay the IRS through EFTPS.

EFTPS is a secure website that is linked to the IRS. It is a payment system through which business owners upload everything in a very secure way – and it’s a vast improvement on the previous system. Payments no longer get lost in the mail or counted incorrectly due to human error. EFTPS is easy to set up a profile and link your bank account; plus, an added security measure allows business owners to set up a second authentication method through a PIN number sent through the mail. Most traditional businesses use EFTPS for payroll tax deposits. Through EFTPS, the employer collects taxes and then sends them on the employee’s behalf, every pay period, which makes it easy for everyone involved. Though, for cannabis operators, it is extremely difficult but not impossible to open a business bank account; therefore, EFTPS is not an option for cannabis companies. Cash can’t be transferred through EFTPS. So as a cannabis operator, how can you pay federal taxes? Federal Taxes for Cannabis Operators

Here’s how cannabis operators can pay their federal taxes in cash.

The first step is to find the location of your nearest IRS office. In California, there are IRS offices located across the state. Maybe 40% of the offices accept cash. We suggest that you call ahead to make an appointment and make sure that your nearest office accepts cash. Give yourself plenty of lead time as there are few IRS offices and they have very few appointments available. And they will not give you a 'break' just because you couldn't get an appointment in time for the deadline, so plan way far ahead. Once you secure an appointment, pack your cash and travel to the office. We recommend you share the appointment day, time, and place with as few people as possible to mitigate the security risk. You will be traveling with a large amount of cash, so don’t increase your chances of being a target. When you go to the office and make a payment, know ahead of time that the IRS office may limit the amount you can pay per appointment. If you’re paying $250,000 in taxes (which is not that uncommon), you will likely need to make many appointments. The reason for this is security; the IRS doesn’t want to take the risk of having a huge amount of cash on the premises. One other thing, make sure you get a receipt each time you pay an installment on your taxes, just in case there’s ever a question down the road. Alternately, some cannabis companies pay their taxes through the business owner’s personal account, and then have the cannabis company reimburse the business owner. This is a work-around that can save a lot of frustration, but also places a financial burden on one individual. Workaround for Small Tax Payments

Some operators may just be getting started and not have a huge tax liability, so here's another method to pay your taxes in cash.

If there’s no IRS office near you that accepts cash, you can pay your taxes in cash at a participating retail store like 7-Eleven. The IRS has a program called PayNearMe that allows you to make a cash payment after being verified. Note that payments are limited to up to $1,000 per day, and can take up to 5 to 7 business days to transmit. Verification also can take two to three business days. Allow yourself plenty of time and review the limitations before committing to this option. Paying State Cannabis Taxes in Cash

The steps for paying your state cannabis taxes in cash are similar to the process for paying your federal taxes.

The agency is different – in California, you will make payments to the franchise tax board – but you will need to find a location near you and set up an appointment. Most offices in California accept cash, but some will even take cashiers checks. Make sure to phone ahead and know what the limitations are before you go. Overall, paying your taxes in cash as a cannabis operators is a burdensome and frustrating process. We can help you strategize and make the most of the limited tax deductions available to cannabis operators. Get in touch with our team by clicking the get started button below.

At the polls earlier this month, voters across the US weighed in on a number of measures related to cannabis. For California voters, midterm results were overwhelmingly in favor of the new adult-use cannabis industry, a good sign for anyone hoping to grow their business venture.

There were about 50 tax measures across the California’s ballots, the majority of which were approved by voters. While more taxes may not necessarily seem like a positive thing to budding entrepreneurs, this is a sign that local governments intend to welcome the cannabis industry and help it grow. It’s to their benefit for businesses to do well, as a local municipality can benefit from the resulting tax revenue. As we go into 2019, here are the new cannabis taxes that companies in California need to pay to stay compliant with state and local laws. San Francisco: Proposition D In San Francisco, voters approved Proposition D, the Marijuana Business Tax Increase. This measure will impose taxes on cannabis ventures that do business in the city, regardless of whether or not their physical site is located there. The tax rates are:

These taxes go into effect in January, 2021 and do not apply to the first $500,000 of recreational cannabis gross receipts. Medical cannabis retail sales are also exempt from this tax. Revenue from this particular tax is expected to reach $5 - $12 million, money which will go into the city’s general use fund. Emeryville: Measure S Emeryville, California voters passed Measure S, a Marijuana Business Tax similar to the one in San Francisco. The business tax measure levies a cannabis business tax of up to 6% of gross receipts. The goal is to generate $2 million in revenue for unrestricted governmental use. This is quite a big leap for Emeryville, as previously cannabis companies paid 0.10% of annual gross receipts, or $25, whichever was greater. The ballot measure does not say when this increased tax rate will go into effect. Oakland: Measure V Oakland, California went in a bit of a different direction when it came to voting on cannabis taxes this November. Voters decided to lower their existing cannabis business tax – though the municipality previously had one of the highest tax rates in the state. Recreational cannabis was taxed at 10%, while medical cannabis companies had a 5% tax rate. Small operators were having a hard time competing in the market with cities nearby charging lower taxes. Measure V was approved by voters to give the Oakland City Council the authority to lower cannabis tax rates through a forthcoming ordinance. The measure also allows cannabis companies to deduct the cost of raw materials from their gross receipts. On the federal level the 280E regulation prevents cannabis companies from doing this on their tax returns. Lastly, this ballot measure allows local cannabis businesses to pay their taxes on a quarterly basis, instead of one annual payment at the beginning of the year. From a tax perspective, Oakland is looking more attractive than ever to entrepreneurs looking to enter the cannabis industry. Lake County: Measure K Lake County’s Measure K Marijuana Business Tax was approved by a majority vote this November. This measure goes into effect January 1, 2021 and changes the following taxes:

Read the full text of the measure to determine where you call in the two tax brackets. Mountain View: Measure Q Mountain View’s Measure Q applies to the maximum of four cannabis businesses allowed to operate in Mountain View, per their permitting regulations. This approved ballot measure imposes up to 9% tax on gross receipts of cannabis businesses. The money will go into a fund for “general city purposes,” estimated to grow to $1 million in annual revenue. Lompoc: Measure D 2018 Lompoc, California voters approved Measure D2018 with the following tax rates to cannabis companies:

Riverbank: Measure B Last but not least, Riverbank voters approved Measure B. This is an interesting step for a municipality that does not currently permit cannabis businesses to operate within their jurisdiction. But, by passing this ballot measure, voters have indicated they are open to allowing adult-use cannabis businesses to operate in the future. Measure B permits Riverbank’s City Council to issue a tax of up to 10% of gross receipts on cannabis businesses operating in the future. Built into the tax are incentives which give the city a cut of any illegal cannabis business earnings. Despite this relatively high tax rate, keep an eye on Riverbank in the future for indications that they may be open to permitting recreational cannabis businesses to operate. If you have any questions about these tax related measures, get in touch with our experts.

As the saying goes, there are two things certain in life: death and taxes. An addendum to this saying might be that taxes never seem to decrease over our lifetime. However, these three California cities have chosen to reduce cannabis taxes in their jurisdiction. Let’s take a look at these three cities and the rates at which they’ve reduced taxes.

Berkeley Berkeley recently hired HdL Companies to audit and review current taxes for cannabis regulations. These services have resulted in a reduction of cannabis taxes within Berkeley. Medicinal sales tax was 5% and is now 2.5%. In addition, adult-use cannabis sales tax was 10% and is now 5%. Salinas Salinas is the largest municipality of Monterey County, California. This city just reduced cannabis nursery tax rates from $15/square foot of canopy space to $2/square foot. If you’re taking the first steps toward starting a cannabis company, this might be a great jurisdiction for you to consider. Grover Beach Grover Beach is a city located in San Luis Obispo County, California. The city recently reduced several taxes related to cannabis, including the cultivation tax from $25 per square foot to $5 per square foot. Manufacturing and distribution taxes have been reduced from 5% of gross receipts to 3%. All taxes for adult-use and medical cannabis remain the same. BONUS: Coalinga Although Coalinga has not officially reduced any of its taxes, the city is looking into the idea of reducing cultivation taxes. The current cultivation tax costs all cannabis businesses at $25.00 per square foot for the first 3,000 square feet. It drops to $10 per square foot after that. We will see what Coalinga decides to do in terms of reducing cultivation taxes. These three cities have reduced cannabis taxes, and depending on the long-term economic growth benefits, it’s likely that other districts could follow suit. We will keep you updated as we see additional cities make changes to their cannabis taxes. Interested in opening a cannabis business of your own within one of these California cities? Contact California Cannabis CPAs today.  The CDTFA released an update recently relating to the cannabis excise tax on CBD products. For a quick refresher on the cannabis excise tax, take a look at our guide for cannabis retailers. As you prepare your cannabis taxes, here’s what you need to know about the excise tax on cannabidiol products.

Cannabis and CBD Products: Definitions Per direction from the CDTFA, "Cannabis" refers to all parts of the Cannabis sativa L. plant, excluding industrial hemp. Likewise, "Cannabis products" refers to cannabis and cannabis plant material that has been processed and transformed into defined as cannabis that has undergone a process that transforms it into a concentrate, edible, topical, or other things that contain cannabis. Does Cannabidiol count as cannabis products? Cannabidiol comes from both the hemp and marijuana varieties of cannabis. In this case, the CDTFA is focused on the marijuana variety: hemp varieties only have small amounts of THC and have been legal in the US for a while. Therefore. CBD products made from industrial hemp are not subject to the cannabis excise tax. Check with the California Department of Food and Agriculture (CDFA) for specific regulations related to the industrial hemp industry. CBD and Excise Tax Regulations Cannabidiol (CBD) products containing "cannabis" are subject to the cannabis excise tax. CBD products that do not contain cannabis are not subject to the cannabis excise tax, even if the CBD product contains trace amounts of Tetrahydrocannabinol (THC). Questions about the excise tax? Get in touch with our experts today!  As spring warms up and nicer weather starts bringing customers out of hibernation, you may be wondering how to increase your sales this season. As a cannabis retailer or manufacturer, one tactic is to offer free cannabis samples to customers to encourage them to try – and buy more of – your product. Is that legal, and what are the tax repercussions of giving away free cannabis? We discuss below.

Can I give away free samples of my cannabis product? First, check to make sure that you can offer free samples legally in your area. You can ask your local officials or ask for guidance guidance from the Bureau of Cannabis Control and the California Department of Public Health. Second, know that these details only apply to licensed manufacturers, not dispensaries. Use Tax and Free Cannabis Samples So, assuming you can legally offer free samples of cannabis, do you have to pay use tax? Remember, use tax is charged on all items that you use or consume and purchased without paying tax. The rate for use tax is the same rate as sales tax. The short answer: yes, you do have to pay use tax when you give away free samples of cannabis. Here’s a more detailed explanation. The use tax comes into play when a product is, literally, “used.” As long as cannabis is part of your inventory being held for sale in the regular course of business, it’s not being used, and therefore you do not pay tax on that supply. When you offer your cannabis product for use – i.e., for a customer to try for free – the use tax will kick in. The tax due on that sample is based on the purchase price by the manufacturer. If you want further details on how this works, read Regulation 1669, Demonstration, Display and Use of Property Held For Resale-General, subdivision (a) as well as Regulation 1670, Gifts, Marketing Aids, Premiums and Prizes. What if I’m offering free samples to employees? Ok, so maybe you’re not so tempted to give away free samples to customers. But what about to your employees? It can be helpful in making a sale to have knowledgeable employees who can personally attest to the quality of your product. So, do you need to pay use tax on cannabis being used for internal promotional purposes? Unfortunately, yes, you still need to pay use tax on free samples given to employees. This still falls under the realm of “use,” as in you are using tangible personal property for any purpose other than demonstration and display. Use tax is measured by the cost of the cannabis product purchase price. Does the use tax rate ever vary? Use tax can vary not by who you are selling cannabis to, or why you are giving it away (e.g. free sample versus normal sale), but by where you sell or give away the cannabis product. The tax rate depends on where the manufacturer gives the sample away. For example, if you give a sample to an employee, the tax applies where the sample was dispensed from (not where the recipient then used the sample). If the sample is given to an employee for personal use, the rate of tax that applies is that of where you made the gift to the employee. Summary and Conclusion While it may be tempting to give away samples of your product for free, note that you will still have to pay use tax on the transition of those samples. The use tax rate that you will pay depends on where the sample was gifted, not where the sample is consumed. Likewise, it doesn’t matter whether you’re offering a sample to an employee or customer; use tax still applies. You may still decide it’s a worthwhile marketing tool to offer a sample, but make sure you are legally allowed to do so before continuing your marketing effort. If you still have questions, check out additional resources in the CDTFA’s Tax Guide for Cannabis Businesses or consult with one of the experts at California Cannabis CPA.  The 2018 tax reform bill passed by Congress brought a lot of new changes to federal taxes for California cannabis businesses. You may have some questions about how to take advantage of these changes, which is why we’re covering all new deductions, liabilities, and tax considerations in ongoing blog updates. Today: should you convert your S-Corp to a C-Corp?

Background: types of business entities As a quick refresher, there are a number of different ways to structure your cannabis business. The way you set-up your new venture has significant tax implications. Here is a quick, high-level overview of some of the most common business structures you might consider forming:

This is a very high level overview of the options available to your business, and if you have specific tax questions for the structure of your cannabis business, we suggest consulting with one of our experts. Let’s move on to the latest tax reforms – and how they impact S-Corps and C-Corps. 2018 Tax Reform Updates Traditionally, small businesses have been encouraged to avoid filing a C-Corporations due to the double taxation issue. S-Corps have always been more appealing business structures for anyone looking for a lower tax rate: typically, individual income tax rates are much lower than business income tax rates. Therefore, especially for small businesses that don’t qualified for the reduced corporate tax rate, setting up a structure where you can claim business income as personal helps owners save money on federal taxes. Congress’s tax reforms in January, 2018 changed that. The tax reforms reduced the corporate tax rate from a maximum of 35% to 20%. Many individual tax rates can reach up to 42%, the tables have turned, and now a 20% tax rate looks more appealing to many business owners who want to avoid paying higher tax rates on their income. Should you convert to a C-Corp? Note that there is some tax relief planned for S-Corps as well. The new tax bill included a temporary provision allowing pass-through entities to deduct up to 20% of their income on their return. This is known as the “qualified business income” deduction (and also applies to partnerships and sole proprietorships). However, this is a temporary provision: and making the switch to the C-Corps would allow your business to access a lower long-term tax rate. Likewise, there are a variety of other deductions that S-Corps and C-Corps businesses can take advantage of. For example, C-Corps can claim the foreign income tax deduction and dividends-received deduction on the repatriation of foreign income where the US Corporation owns 100% of the foreign company. The latest tax reform suggests the current administration and Congress is doing its best to ease regulations on traditional corporations – something your cannabis startup may inevitably benefit from. How do you convert to a C-Corps? It’s relatively straightforward to convert an existing company to a C-Corporation in California. The process starts when you file a set of articles of incorporation with the California Secretary of State. You can read more about the process on the California Franchise Tax Board website. Of course, before making any major business decisions, we recommend consulting with an expert to understand the full implications of your tax liability and business obligations. Filing as a C-Corps may lead to tax benefits, but this business entity comes with lots of other responsibilities.  The recent tax reform law passed by Congress has brought a ton of new changes – and new opportunities – for businesses looking for tax deductions this year. Read our recent updates on changes to the international income tax deduction and the corporate dividends received deduction. This week, we’re covering the Qualified Business Income (QBI) Deduction. What is the QBI? Under the new tax law passed by Congress in January, 2018, certain types of business entities are entitled to take a 20% deduction on “qualified business income” earned. These entities include:

What is qualified business income? Basically, it’s the ordinary, non-investment income your business generates. Think of it as your revenue from sales, without things like interest or dividend income or any other gains from sale of property. It also excluded earned income like salaries and guaranteed payment. Before you start celebrating what looks like a lot of free money, note that the deduction is limited to the lesser of EITHER 20% of qualified business income, or 50% of the total W-2 wages paid by the business. Here’s an example of the MAJOR impact the QBI can have on your tax return (its an over simplified version for ease of explanation):

The fine print: this limitation does not apply for taxpayers below the following threshold amounts. Likewise, this table is a bit of an oversimplification of a complicated deduction. To fully understand if your business can claim QBI, contact one of our experts.

These amounts are indexed for cost-of-living adjustments in $50 increments. How to take advantage of the QBI Deduction As previously noted, the QBI can only be claimed by certain business entities. Cannabis companies that have registered as partnerships, S corporations, or sole proprietorships may be able to take advantage of the QBI. Registering your business as one of these entities gives you a competitive tax advantage over C corporations, as well as a competitive advantage over employees. Its important to structure your business in a way that can allow maximum deductions. The QBI deduction can get complicated pretty quickly, so if you want to take advantage of this deduction on your taxes this year, get in touch with the experts at California Cannabis CPAs. Lastly, please note that the QBI deduction will not apply after 2025. Therefore, if you’re interested in taking advantage of this deduction, now is the time! It also means that you shouldn’t structure your entire business around this one deduction: if none of these business entities feel right for your particular needs, it’s not worth changing your entire business model to suit a deduction that expires in 2026. If you do decide an S Corp, sole proprietorship, or partnership is right for you, consult with our experts to make sure your company is structured appropriately to take advantage of the QBI.  Nearly three months into the legalization of cannabis in California, and we’re still covering state updates to taxes related to running a cannabis business. This is a big update for dispensary owners located in Los Angeles – and impacts how you pay your city taxes. Today’s post: Los Angeles’ updates to the existing L050 Medical Marijuana business tax classification. As of January, 2018, the previous business tax classification was replaced by the following rates.

For more on cannabis taxes for retailers and cannabis cultivators, check out our blog series on cannabis taxes.

When do you need to pay these taxes? These tax payments are due on a quarterly basis starting in January 2018. To give businesses time to adjust, any activities related to the first quarter of 2018 (January, February, March) and the 2nd quarter of 2018 (April, May, June) will be both due on July 1, 2018. After that, quarters will be due after the last day of that quarter. For example the 3rd quarter of 2018 will be due October 1, 2018. In July 2019, the schedule will change to reporting on a monthly basis. How do you report these taxes? Look for tax certificates to come in the mail from the Office of Finances within 3 to 4 weeks after registering as a business. These business tax registrations certificates (BTRC’s) are for the purpose of business tax compliance, and you should not consider them as your permit to begin operating as a cannabis business. For more information about these business tax classifications please refer to the Los Angeles Municipal Code sections 21.51 and 21.52 or get in touch with the experts at California Cannabis CPA.  We’re back from our coverage of Michigan’s medical cannabis licensing updates with more tax law changes that may benefit your cannabis business. As CPAs we want to help your small business understand the implications of the new 2018 tax plan and figure out how to get the most from your tax return. Today’s topic: corporate changes for international taxes. Of course, if you have specific questions, please reach out to an expert at California Cannabis CPAs.

Background on the Federal Income Tax Before giving you an update on the changes, let’s first have a quick recap of how US taxpayers have traditionally reported their income tax. Current law mandates the US taxpayer report their worldwide income and offers a foreign tax credit for any taxes paid overseas. For example, if you went on a trip to Europe for three months and worked during that time, you will be taxed on that income by the US government. You may also have paid taxes on that income to the country in which you worked, in which case you would receive a credit from the US compensating you for that amount. Historically, this rule has been applied to corporations as well. Foreign income earned by a foreign corporation that is owned by a US citizen was not subject to US taxes, unless the income was distributed in the form of a dividend. Changes to the International Income Tax The new law deploys a “territorial” income tax system. Under this system, companies are only taxed on their US earnings, meaning that any foreign income can be excluded from your income report. Why? The goal of the new law is to encourage companies to bring their profits back to the US. The new provisions incentivize the repatriation of foreign income to the US with tax-free status. Cash repatriated back to the US will be untaxed when the transfer takes place, however no foreign tax credit is allowed for taxes paid overseas. Essentially, this is both a carrot and stick approach to bringing your profits stateside. If you bring your cash back to the US economy, you’re rewarded with tax-free status. If you don’t, the US will no longer be reimbursing international taxes. International Income Tax: The Details As with any tax law, the new bill includes many provisions to ensure that corporations do not have excess untaxed returns on earnings from low tax jurisdictions:

It’s also important to note that C-Corporations will get a 100% dividends-received deduction on the repatriation of foreign income in the future where the US Corporation owns 100% of the foreign company. What does this mean for your cannabis business? If you’re just starting to form a business and considering what business structure is right for your cannabis business, a C Corporation may look more appealing. In addition to being able to take advantage of the DRD, a C Corporation has many benefits if you’re looking to eventually expand internationally. And international expansion might be the next big move for cannabis companies: the California is in good company with 20 other countries that have legalized cannabis to some degree. Besides commonly known places like The Netherlands, Uruguay, Peru, and Jamaica all have cannabis legalization rules in the books. Likewise, Germany, Spain, Portugal and the Czech Republic are all weed-friendly communities well on their way to full legalization. If you’re looking to diversify your customer base, consider expanding outside of US borders. Curious what other deductions the new tax law holds? Talk to one of our experts or sign up for our email newsletter for new updates each week.  Tax season is well underway: are you ready? We’re starting a series to help cannabis companies understand how the recent tax reforms passed by Congress will impact your tax obligations. Like many small businesses, the intricacies of the new tax plan have big implications for California cannabis companies. From what you can deduct on your tax return to what you need to be responsible for moving forward, we’re here to help you catch up. If you have specific questions, please reach out to an expert at California Cannabis CPAs. What is a DRD? DRD stands for Dividends Received Deduction. This is a federal tax deduction that certain corporations – ones that receive dividends – can take. The goal of the DRD is to prevent the same income from being taxed three times. The DRD makes it so that if Company A receives a dividend payout from Company B, Company A can claim that dividend as income and accordingly receive an income tax reduction. How much can you claim on your DRD? DRD is a little more complex than it may seem at first glance. The deduction amount that a company may claim depends on its percentage of ownership in the company paying the dividend. For example, if Company A owns a 20% stake in Company B, and Company C owns a 60% stake in Company B, Companies A and C will be able to claim different amounts of DRD. The amounts are based on their ownership stake. As of 2018 and the changes in the tax law, the percentage DRD a company can claim changed: Current DRD

Effective for years beginning after 12/31/17, the 70% DRD will be reduced to 50% and the 80% DRD will change to 65%.

The Fine Print There are a few key limitations to know, including the taxable income limitation and the timeline for owning shares limitation.

What this means for Cannabis Companies It’s not uncommon for our experts to see a cannabis holding company (the company which a main investor will agree to fund) operate with a subsidiary (e.g., a real estate company, operating company, or management company). Creating a structure that allows you to maximize your DRD will decrease your overall effective tax rate and increase your cash flows to re-invest in your companies. Be aware of the latest changes in the tax code if you want your company to survive in the new highly taxed marketplace. Specific questions? Get in touch with our experts today to make sure you’re claiming your full deductions on this year’s tax return and mitigate the possibility of overpaying your taxes.  2018 and the new tax code presents itself with a myriad of changes on both an individual and corporate level. One of the biggest changes, from a corporate level, was the elimination of the AMT (Alternative Minimum Tax). Today, we will talk about the definition of AMT, why it started and how it will impact the cannabis industry.

What is AMT? The corporate Alternative Minimum Tax (AMT) is a separate and distinct method of taxation that runs parallel to the “regular” corporate income tax. Prior to 2018, every corporation had to calculate its tax burden under both the regular corporate income tax and the AMT, paying the higher of the two. It’s important to note, today we will strictly be talking about AMT as it relates to corporations, not individuals (the AMT was not eliminated for individuals). The Alternative Minimum Tax began in 1969. The start of AMT can be traced to then Secretary of Treasury Joseph W. Barr. He testified before Congress that 155 individual taxpayers, with incomes exceeding $200,000, had paid no federal income tax in 1966. Adjusted for inflation, those numbers would translate to $1.5 million dollars today. The idea that the wealthiest citizens could pay zero income tax did not sit well with the government. Therefore, the AMT was created. This ensured that even those with higher incomes would pay a minimum amount of tax. Otherwise, through tax deductions and credits, citizens could essentially pay zero taxes. With so many deductions available, lawmakers wanted to ensure everyone paid at least some base minimum of tax regardless of how many tax breaks they could use to their advantage. Changes For 2018 Prior to the changes of 2018, the United States had one of the highest corporate tax rates in the world at 35%. The new 2018 regulations establish a flat 21% corporate rate for businesses and personal service corporations (PSCs). The corporate tax rate average for the developed world is 22%. Theoretically, the reduction of the corporate tax rate by 14% should create a nice boom for U.S. based companies, allowing them to keep their operations and profits here in the U.S. Prior to the changes for 2018, the corporate AMT tax rate was 20 percent. Additionally, C corporations with average gross receipts less than $7.5 million over the preceding three tax years were not subject to AMT. As of January 1, 2018 – the corporate AMT was completely eliminated. Individual AMT still applies, although a few things have changed. Please consult California Cannabis CPA if you’d like some guidance on individual AMT regulations. How Do These Changes Affect The Cannabis Industry? If your cannabis business is a corporation, you may benefit from the elimination of the AMT. If you are still researching how to set up your business, read our 10 steps to start a cannabis business. California Cannabis CPA is happy to walk you through the process. Theoretically, the removal of AMT should be a benefit. The AMT was a completely separate tax code that created a lot of additional record keeping. The elimination simplifies dozens of other tax code sections that were related to the corporate AMT. And unlike before, if your business made over a certain amount of money, you had to pay the higher of the two taxes. Not the case anymore. Second, functioning businesses are able to write off (or deduct) certain business expenses from their overall income. Normally, these include expenses such as operating costs, employee expenses and equipment. However, the cannabis business has certain limitations due to tax code 280E. On the federal level, cannabis is still considered a Schedule 1 drug. Therefore, licensed marijuana businesses have to file federal taxes under tax code 280E because of the Controlled Substances Act. The downside to filing under 280E is that licensed cannabis businesses pay more in federal taxes than other businesses do. 280E bans any tax deductions besides the cost of goods sold. If you try to deduct other expenses (similar to how other businesses operate) you will likely face an audit. However, there are situations where additional write-offs may be allowed. This is usually the case if your business participates in marijuana for medicinal purposes. 280E is a very complicated tax code, so we recommend consulting with California Cannabis CPA to ensure every detail is covered. In conclusion, it looks like the removal of the AMT will be beneficial, but cannabis companies will still run into challenges with the amount of expenses they are able to deduct. California Cannabis CPA is happy to speak with you to discuss your individual circumstance, ensuring you remain compliant with the new tax codes.

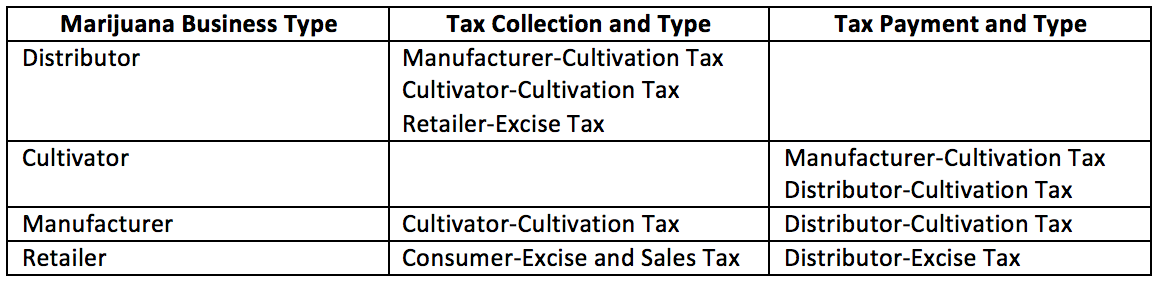

We’ve offered guides for cannabis retailers and cannabis distributors, and here we cover tax responsibilities for cannabis cultivators and manufacturers. If you’ve been following our guides, many of these responsibilities will be familiar. Cannabis cultivators are anyone who grow, harvest, plant, dry, cure, grade, or trim the cannabis plant. If you are a nursery or cannabis plant processor, you are considered a cultivator. If you are someone who produces or prepares cannabis products, labels or re-labels cannabis containers, or who packages/repackages cannabis products, you are a manufacturer. Cultivators have to register for a seller’s permit with the CDTFA online at cdtfa.ca.gov. As a cultivator, when you make sales to other cannabis businesses, you will be required to get resale certificates, file sales and use tax returns, and report and pay use tax on taxable items purchased without tax and used by the cultivator. In addition, cannabis cultivators pay the cultivation tax to the distributor or manufacturer. In cases where unprocessed cannabis is first sold or transferred to a manufacturer, the manufacturer must collect the cultivation tax from the cultivator and pass it to the distributor for collection by the CDFTA. As a manufacturer, your responsibilities are similar to cultivators. You must also register for a seller’s permit, obtain resale certificates, file sales and use tax returns, and report and pay use tax on taxable items on taxable items purchased without tax and used by the manufacturer. Likewise, you are responsible for collecting cultivation tax from the cultivators and supplying a receipt if the unprocessed cannabis is transferred or sold to you first. Then, you will pay the cultivation tax to the distributor, who transfers the payment to the CDTFA. Be sure you keep proper records and have the right permits and licenses – in addition to a seller’s permit, both cultivators and manufacturers may need local or municipal-level licenses. We can help you sort out your licensing needs. Cultivation Tax This tax applies to all harvested cannabis that has entered the commercial market: that is, cannabis that has completed testing and complies with the quality assurance review as required by law. How much is cultivation tax? It depends on the type of cannabis products being sold.

*Fresh cannabis plant fee only applies when the cannabis plant is weighed in an unprocessed state within 2 hours of harvesting. If you have immediate questions, please get in touch with our experts. Once again, distributors collect the cultivation tax from cultivators and manufacturers. Tax is due when the cannabis enters the commercial market. The distributor will provide an invoice or receipt when they collect the cultivation tax, and you should keep this for your records. Sales and Use Tax File your sales and use tax returns separate from your cannabis and income tax returns. Sales and use tax returns should be filed on the CDTFA website based on the due dates, which may vary. There are also some prepayments you will be asked to make which can be found on the same site. Keep copies of your returns in case there’s ever a question on your record-keeping. Sales tax applies to the retail sales of tangible personal property, including some labor or service costs if they are related to the sale of tangible property. Sales tax does not apply to valid sales for resale, though, so as a cultivator or manufacturer, virtually all your sales should be for resale (meaning your sales tax responsibilities are negligible). When you make a resale, use Form CDTFA-230 as your resale certificate. Don’t use a resale certificate for any personal property – you may be penalized! Use tax is a tax on all items that you use and consume and purchased without paying tax. In the real world, this might include getting a massage – it was a service you used that likely didn’t include tax when you originally paid the masseuse. Use tax is the same rate as sales tax and will generally apply to purchased from outside California that you didn’t pay state tax on at the time of purchase. These tax responsibilities can seem overwhelming, but that’s where our experts come in to help. If you have any questions pertaining to cultivation, sales, or use tax, please don’t hesitate to get in touch. We’re here to help you stay compliant!  Leading up to 2018, the CDTFA passed two key regulations clarifying their requirements for correctly paying your cannabis cultivation and excise taxes. Regulations 3700 and 3701 pertain to collecting tax on inventory you’ve had in stock before the full legalization of cannabis in California, and are important to understand before filing your first-quarter report on April 30, 2018.

Cannabis Tax Regulation 3700: Cannabis Excise and Cultivation Taxes Passed in December, 2017, this regulation clarified the existing excise and cultivation tax policy everyone must follow starting January 1, 2018. Specifically, this regulation clearly defines terms such as “fresh cannabis plant,” “distributor,” “cultivator,” and cannabis leaves and flowers. It also lays out the cultivation tax rates, which we’ve covered in previous articles. Perhaps most importantly, Regulation 3700 also lays out the process for collecting the cannabis excise tax. Distributors are responsible for collecting, reporting and remitting cannabis excise tax from the cultivators and retailers each quarter. Late payments incur the following penalties:

However, if the CDTFA finds that a failure to make a timely payment is due to reasonable cause, you may be relieved of penalty. To be relieved, you must prove that payment was late due to circumstances beyond the person’s control, and occurred in absence of willful neglect. If you find yourself in this situation, it’s best to consult with a tax or law expert to file a statement explaining the facts pertaining to your claim. Cannabis Tax Regulation 3701: Collection and Remittance of the Cannabis Excise Tax After passing Regulation 3700, California officials discovered a loophole to the cannabis excise tax– which regulation 3701 aims to close. Prior to the full legalization of cannabis in California, no person was required to obtain a distributor license until January 1, 2018. However, there were certainly individuals and companies operating as distributors before January 1 – distributors in the medical cannabis industry, for example. These companies would have existing cannabis inventory – so should this inventory be subject to the new cannabis excise tax? Regulation 3701 says that if a retailer possesses or controls cannabis or a cannabis product at 12:01 a.m. on January 1, 2018, and makes a retail sale of that cannabis or cannabis product on or after January 1, 2018, then that retailer must charge a cannabis excise tax based on the average market price. This excise tax is due to the distributor by the fifteenth day of the calendar month following the close of the calendar month in which the tax was collected. Here’s how this works in practice. A retailer purchases cannabis in 2017, and on January 3, 2018, purchases cannabis from a distributor for $100/oz. The wholesale cost is $100/oz. Therefore, the average market prices of an ounce is $160.00 ($100 x 1.6). The cannabis excise tax due on the sale of the cannabis purchased in 2017 is $24.00 ($160 x 15%) and the retailer must collect this excise tax from its customer. Lastly, distributors need to know how to report the pre-2018 excise tax. When remitting the excise tax to the CDTFA, distributors should include the following information:

Include this information on your first quarter tax return, due April 30, 2018. Questions? Get in touch, we’re happy to help.  Continuing our series from last week, today we’re covering the key tax policy that cannabis distributors in California are responsible for now that proposition 64 has been approved. If you’re a retailer looking for detailed tax information, check out this for California cannabis retailers.

Distributors are also responsible for collecting and submitting a variety of taxes, including cannabis cultivation, sales, excise, and use taxes. Distributors are also responsible for filing the cannabis taxes after collecting cultivation and excise tax from the retailers and cultivators, and for keeping resale certificates on file from retailers. Here’s how to file your taxes, how much to collect from your cannabis partners, and how to handle sales tax. Please consider that we are not a law firm, and this advice should not substitute any proper legal advice. Are you a cannabis distributor? You are cannabis distributor if you procure, sell and/or transport cannabis between licensed cannabis businesses such as cultivators, manufacturers or retailers. Distributors must meet also meet the following requirements:

If you are also making sales, and not just transporting product, you are responsible for registering with the CDTFA to get a separate seller’s permit. This will also require filing Sales and Use Tax Returns. Are you a microbusiness? This complicates things a little. Microbusinesses may operate as a distributor, but in that case they are only required to hold one license that authorizes the microbusiness as a distributor. A microbusiness may operate as a cultivator, distributor, manufacturer and/or retailer. Microbusinesses are responsible for all of the same requirements as distributor requirements listed above. Distributor Cannabis Tax Requirements CULTIVATION TAX As a refresher, The cultivation tax is imposed imposed on all of the harvested cannabis that enters the commercial market. Cultivators are responsible for paying the cultivation tax to the distributor. In some cases, the cultivator is responsible for paying the tax to the manufacturer if the cannabis is transferred or sold to a manufacturer first. Either way, as a distributor, you are responsible for remitting the cultivation tax to the CDTFA. Cultivation tax rates are:

To qualify for the third point, the cannabis plant must be weighed in an unprocessed state within 2 hours of harvesting. If you have immediate questions, please get in touch with our experts. When you collect the cultivation tax, you will need to provide a receipt to the cultivators and manufacturers that lists the amount of the tax collected and relieves your cannabis partners from liability. CANNABIS EXCISE TAX Excise tax is a bit complicated: put most simply, excise tax is an added 15% of the average market price to the listed retail price of the cannabis product. It’s also contingent on the type of transaction between the customer and retailer. Read more about the cannabis excise tax under our post for retailers. FILING YOUR CANNABIS TAX RETURN The process for filing your cannabis tax return is slightly different from filing your income tax return and sales and use tax return. File your return on the CDTFA.gov site according to the quarterly schedule (so, your first return is due April 30). On this return, you are responsible for reporting the both the excise and cultivation taxes due for any cannabis and cannabis products that entered the commercial market during the reporting period. For example, on your April 30 return, you will report excise and cultivation taxes for January 1 – March 30, 2018. When reporting the excise tax, you must include reports for any product that has been transferred to a retailer (whether or not the product has already been sold). Keep copies of your returns for future reference, and speak to one of our experts if you have any help. Distributor Excise Tax Requirements CANNABIS EXCISE TAX As a distributor, you are responsible for paying the cannabis excise tax to the CDTFA and collecting it from your retailers you supply. Sales tax does not apply to valid sales for resale. Unless you’re operating as a cannabis microbusiness, your sales as a cannabis distributor are likely to be all resale – meaning you won’t be responsible for paying sales tax. Enter: resale certificates. Resale certificates allow you to buy resale inventory without paying sales tax reimbursement to the seller. You must provide a timely resale certificate to your supplier, with your seller’s permit information at the time you are making your purchases. Use Form CDTFA-230 as your resale certificate. Don’t use a resale certificate for any personal property – you may be penalized. Also, when you sell products to retailers, those retailers will give you a resale certificate that you should keep for your records. If you have any questions about using the resale certificate, get in touch! We’re happy to help. Retailer Sales Tax Requirements CANNABIS SALES TAX Retailers will collect the sales tax from their customers and remit it to the CDTFA. The sales tax rate is based on where your sale takes place. To find the correct tax rate, check the database on the CDTFA site.  As we previously discussed, there are some key taxes with retailers and distributors must know about to stay compliant with California cannabis regulations. The two we’re outlining in this guide are the cannabis sales tax, and the cannabis excise tax.

Cannabis Sales Tax Retailers are primarily responsible for the sales tax, which applies to all “tangible personal property” in California – including cannabis, cannabis products, and cannabis accessories (rolling papers, vape pens, etc.). To calculate the amount of sales tax, use the total amount on your receipts (including the excise tax). The sales tax rate is based on where your sale takes place. Is it a sale that takes place over the counter in your store, or when you deliver the product yourself? For example, if you sell cannabis at your store location in Los Angeles, you may have a different sales tax than if you make a delivery to a customer in San Diego. To find the correct tax rate, check the database on the CDTFA site. Why are the tax rates variable by location? This is because the sales tax has three key components:

Check with your local municipality for your sales tax rate. Note that certain medicinal cannabis sales are exempt from sales tax. A customer is exempt from paying sales tax when they present a valid Medical Marijuana Identification card (issued by the California Department of Public Health), along with a valid government ID. Be careful: a doctor’s note or prescription isn’t sufficient for that customer to qualify for sales tax exemption. Keep track of these transactions – you’ll need to report any sales tax exemptions when you file your taxes! If you need help, give us a call or get in touch for a quick consultation. Cannabis Excise Tax Retailers and microbusinesses must collect an excise tax from their customers. As we outlined in this brief explainer for cannabis retailers, an excise tax is usually included in the price of the product, so you collect this tax from your customers every time you make a sale. Charge excise tax on everything from cannabis to cannabis edibles, oils, lotions, and waxes. How much should your excise tax be? The short answer: add on an extra 15% of the average market price to the listed retail price of your product. The average market price is based on the type of transaction between the seller and you. There are two types of transactions for you to know about:

Once you have determined whether you’re dealing with an arm’s length or non-arm’s length transaction, you can figure out how much your excise tax should cost. Check with your local municipality for your local excise tax rate. Here’s an example. You are a Los Angeles dispensary selling cannabis directly to a customer in an arm’s length transaction. The sale of one gram of cannabis is $20. On top of that, you charge an excise tax at 15% - so the sale goes to $23. Then you have to add Los Angeles sales tax (9.75%). The total out the door price is therefore $25.25. While this sounds complicated, the end result is simple. You are not required to list the excise tax separately on your receipt. However, you must have the phrase “The cannabis excise taxes are included in the total amount of this invoice” included on every receipt. Questions about the sales and excise tax rates? Get in touch – our experts are happy to help.  While we’re not a law firm and cannot provide legal advice, there are a few key tax laws that cannabis retailers in California are responsible for now that cannabis is legal. The goal of this article is to give you an overview of these taxes and make you aware of your responsibilities as a cannabis business owner in California. In subsequent posts, we’ll dig into the excise, sales, and use taxes to give you everything you need to know about these tax requirements – and make sure your business stays compliant. For now, here are the basics you need to know.

Are you a cannabis retailer? You are a retailer if you sell cannabis and/or cannabis products directly to a consumer. Microbusinesses that are licensed as retailers also must abide by the same regulations as traditional retailers. A cannabis microbusiness is type of license category (Type 12) that allows your company to engage in multiple cannabis activities at one location. For example, as a microbusiness you could cultivate up to 10,000 sq. ft. of cannabis canopy and distribute your product under one license. Because often you are selling your product to a consumer, these microbusinesses follow the same regulations as retailers (detailed here). If you’re not sure whether you’re a cannabis retailer, get in touch with California Cannabis CPAs. First Steps to Becoming a Cannabis Retailer Before we dive into the tax law basics, a quick refresh: to be a cannabis retailer in California, you must start by applying for a seller’s permit and also secure local and state cannabis permits. Click this link to register with the CDTFA for a seller's permit. For details on what you need to get a seller’s permit – including a checklist of the documents you need to submit in your application – check out this blog post. Please keep in mind that you may be responsible for getting additional permits and licenses from your local county or city government. More on that to come! Next, if you are an existing cannabis retailer (i.e., not a new company) you are also required to report all your sales and pay sales tax due to the California Department of Tax and Fee Administration (CDTFA). The amount of tax you’ll pay is based on your gross receipts, meaning the tax rate is set based on where the sale takes place and when the sale is over the counter vs. when you deliver the item yourself. Finally, keep in mind that as you grow your business, you will be taxed on items you use that are purchased without tax – so hold onto your receipts and keep track of your inventory. Retailer Tax Law Basics There are a few key taxes that retailers are responsible for as of January 1, 2018. Cultivation Tax Anyone who cultivates cannabis is responsible for paying a cultivation tax – including retailers who grow their own cannabis. Pay this tax to the distributor in a similar process to the excise tax collection. Current cultivation tax rates are $9.25 per dry-weight ounce of cannabis flowers, as well as a tax of $2.75 per dry-weight ounce of cannabis leaves. Exempt from the cultivation tax are businesses that cultivate cannabis for personal use or by a qualified patient or primary caregiver -- i.e., medical cannabis cultivators. Cannabis Excise Tax An excise tax is a fancy name for a tax paid when purchases are made on a specific good – like cannabis and cannabis related products. The excise tax is usually included in the price of the product, meaning you’ll collect this tax from your customers every time you make a sale. Charge excise tax on everything from cannabis to cannabis edibles, oils, lotions, and waxes. How much should excise tax be? Add on an extra 15% of the average market price to the listed retail price of your product. The average market price is based on the type of transaction between the seller and you. We will dig into this in detail later on. Note that you are not required to list the excise tax separately on your receipt – this makes it much easier for you to pay your sales tax, as you will see in the following section. You do need to have the phrase “The cannabis excise taxes are included in the total amount of this invoice” included on every receipt. Sales Tax There remains an exemption for sales and use tax for all medicinal cannabis products, but usually, as a retailer, you will need to pay sales tax. Sales tax applies to retail sales of “tangible personal property” in California – in plain terms, this means anything you can touch and feel, including cannabis, cannabis products, and cannabis accessories such as rolling papers, vape pens, or pipes. When calculating the amount of sales tax due, you must include the amount of your excise tax in the receipts. Since the excise tax should be included in your total sales price, this shouldn’t require any additional effort from you in totally your gross sales tax. You are liable for sales tax even if you don’t collect sales tax reimbursement. This means you must pay the excise tax even if you don’t sell the product. How much is your sales tax? That depends. The sales tax rate is based on where your sale takes place when it is over the counter, or when you deliver the product yourself. So, for example, if you sell cannabis at your store location in Los Angeles, you may have a different sales tax than if you make a delivery to a customer in San Diego. All tax rates are on the CDTFA website – and more on this tax to come. Use Tax Use tax is a tax on items you use or consume that you purchased without paying tax. An example of a use tax in everyday life might be a tax on getting a massage. The use tax rate is the same rate as your sales tax rate. Broadly, expect to pay use tax on items you purchased outside the state of California without paying California state sales or use tax. If this sounds confusing, it is. We’ll cover in greater detail what kinds of products you can expect to pay use tax on in future posts. In the meantime, if you have any questions, don’t hesitate to reach out to the experts at California Cannabis CPAs!  Happy New Year and welcome to a world where cannabis is officially legal in the state of California! We hope this year brings big things for your business. To help you stay on track, we’re helping you start off the year right with a checklist of all the forms your business will need come tax time. Whether you’re filing for the first time or a seasoned pro, take a look at this list to make sure your business is prepared. Questions? The experts at California Cannabis CPAs are here to help. Just let us know! What you Need to File Your Taxes Cultivators and retailers of cannabis products must pay a cultivation and excise tax to the distributor. Distributors are required to electronically file a tax return with the CDTFA on the last day of the month following the reporting period. This is where you file both the cannabis taxes and sales taxes. To file your return, you need the following things:

Check out the graphic below for a breakdown of collected taxes from commercial cannabis businesses in California.  California state taxes for cannabis cultivators, retailers, and distributors go into effect on January 1, 2018. Here's what you will be responsible for paying. State vs. Federal Taxes for California Cannabis Companies

Starting in this month, California is introducing a 15% state excise tax on every purchase of a cannabis product. Retailers are required to charge that tax on customers at the point of sale -- and you will need to keep track and report that accounting when you file your own taxes. Likewise, it will be mission critical to keep track of the California licenses and permits you need before tax time. The cultivation and excise taxes will be collected by distributors from cultivators and retailers and paid to the California Department of Tax and Fee Administration. As for the federal tax system, your cannabis business should file an income tax return just like any other business. What you file will depend on your business entity -- the way you’re structured. For example, a corporation would file a Form 100, California Corporation Franchise Tax or Income Tax Return. The main difference in filing your taxes will be in the deductions, credits and records you’ll be asked to submit at the time of your filling. To convert your nonprofit cannabis company into a for-profit, check out this guide. Or, if you’re just getting started setting up your business structure, you may want to take these tax ramifications into account. Local Taxes Not only will you have California state taxes, but there are also local taxes and fees to pay. Cities and counties may impose additional taxes to produce revenue for their community, and fluctuating tax rates depend on where your cannabis company operates and is located. To find your local tax regulations, contact your municipality. Have questions about being prepared for tax time? Get in touch, we’re happy to help! How to convert your cannabis nonprofit into a for-profit (and put more money in your pocket)12/18/2017

There’s more big news for cannabis businesses as we roll closer to 2018 and the start of legal cannabis in California! Existing cannabis nonprofits who wish to convert to a for-profit entity can file with the California Secretary of State to do so starting January 1.

Why would you consider converting a non-profit to a for-profit? There are two big drawbacks to being a non-profit to consider:

Therefore, if you’re interested in building a business and selling it, or making a profit that you don’t need to reinvest back into your business, a for-profit would be the way to go. Sound like a promising model? Here’s what you need to know to convert your cannabis non-profit into a for-profit. Who does this apply to? First, remember that everyone starting a cannabis business in California needs to file with the Secretary of State. Specifically, entrepreneurs seeking to start a cannabis-related business in need to register their business entity, as well as any trademark or service mark. Next, if you’re an existing nonprofit -- a mutual benefit corporation or a cooperative corporation -- and you wish to convert to a for-profit entity, you must register this change with the Secretary of State starting January 1, 2018. This applies to any businesses looking to become a Corporation, Limited Liability Company (LLC), Limited Partnership (LP) or limited Liability Partnership (LLP). If you’re a new business, you are required to register with the Secretary of State before applying for any license(s) with other local and state agencies. Not sure what business structure is right for you? Luckily, there’s a guide for that. The California Secretary of State has this overview of the different forms your canna-business can take. Of course, if you have any questions about the differences between a corporation, LLC, LP, or any of the other options, GreenGrowth CPAs are here to help. Steps for Registering Your Cannabis Business The office of the Secretary of State has set up an online portal to make the process of registering your business relatively straightforward. (And if you like Cheech, there’s a great PSA to go with the new site that you should definitely watch.) Follow these simple steps to get your business registered correctly.

This is a lot information to take in, and if you’re feeling overwhelmed, GreenGrowth CPAs are here to help. Get in touch with any questions and we’ll guide you through the registration process.  EMERGENCY RELEASE: CALIFORNIA CANNABIS DISPENSARIES MUST PAY TAXES BEFORE GETTING SELLERS PERMIT

What happened: In news this week, California’s Department of Tax and Fee Administration is requesting dispensaries to pay any unpaid taxes before getting a seller’s permit. It’s an effort to bring those gray-area operators who haven’t formally been paying taxes up to code before the marijuana industry takes off in 2018. For any businesses already growing or selling cannabis, the California state government will request that all dispensaries must pay their taxes before applying for a sellers permit. Why is it important: The cannabis industry in California is projected to bring in $1 billion in taxes by 2020, and the government wants to kickstart that windfall early. Not only that, but regulators are hoping to quash any lingering black market operators. The goal in requiring operators to pay back-taxes is to bring the industry above board before January 1 -- not to punish any existing operators, says one expert. Therefore, the state is likely to continue to work with any business owners who still want to get a seller’s permit and haven’t yet paid their taxes. What you need to do now: If you’re one of those gray areas operators, start to go through your records to determine how much tax you potentially owe before January 1. Under the state’s recent legislation, retailers and growers need temporary business permits from their individual towns or jurisdictions. These permits will last for four months, at which point they will be approved by state regulators for the official seller’s permit. That means now is the time to catch up on any lingering back taxes -- or risk getting shut down four months from now. Questions on how this applies to you? Get in touch with the experts at California Cannabis CPA today to get some advice on how to best proceed for your canna-business. We can help you easily get caught up on your taxes and get your return filed in a week!  So, you want to start a business in California’s booming cannabis industry. Now seems like the perfect time to get in on the ground floor: the market estimates that cannabis will bring an additional $5 billion to California each year. It would be nice to get a slice of that pie, no?

Before you dive in, take some time to learn about the different ways to structure your business in a way that will give you the biggest slice of the pie -- not the leftover sliver that’s all crust (unless crust is your thing). The way you setup your company can mean the difference between growth and success and burning out after a year in business. Ask these five tax questions when setting out to structure your canna-business! 1. What kind of legal entity do you want to be? Historically, before California decided to have a fully regulated state system for medical marijuana, cannabis companies were set up as non-profits. Now, there are other options for structuring your business. Figuring out which model is right for you depends on many factors, including your role in the cannabis industry (i.e. grower, distributor, or partner); county and local regulations; and your projected growth. Here are some options available: Nonprofit (allowed pre-2018):

For profit (allowed in 2018):